Downsizing In Retirement: A Step-by-Step Guide

Alder Terrace Gardens

For more information about the author, click to view their website: https://alderterrace.org/

Mar 26, 2024

Florida - Sarasota, Bradenton & Charlotte Counties

Email US

Click to Email UsMillions of older Americans are choosing to go small in retirement.

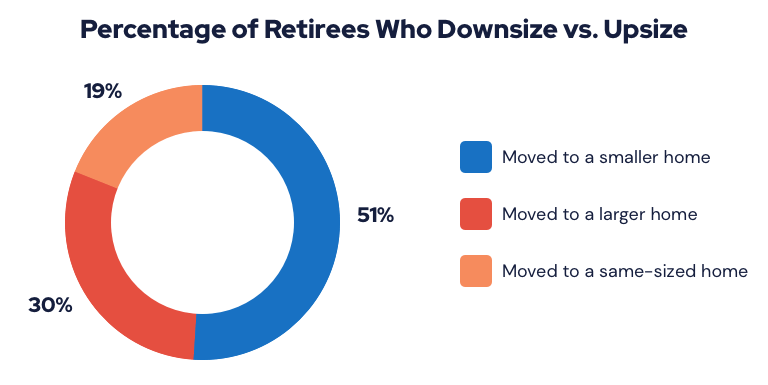

According to a Zillow report, 46 percent of baby boomers who sold homes in 2017 were in the process of downsizing.

Downsizing is a major decision, influenced by unique financial and emotional factors.

Decluttering a large home is no easy feat. Selling your house, finding a new one and moving your belongings adds further complexity.

In this guide, we explore the reasons people downsize for retirement and share advice from experts on how to navigate the transition.

We also look at other aspects of the process, such as getting your home market-ready and estimating moving costs.

Determine Your Reasons for Moving

Moving is a stressful experience at any age. Downsizing for retirement carries unique challenges.

Before you get started, determine why you’re moving.

In a 2018 study by Merrill Lynch, the number one reason given by respondents for moving in retirement was to be closer to family. The desire to reduce expenses came in a close second.

Not everyone makes the conscious decision to downsize. Sometimes a move is immediate and necessary because of rapidly declining health, the loss of a spouse or an unexpected financial crisis.

Understand your own motivation for moving. Weigh the pros and cons so that you feel comfortable with the decision.

- Where do you want to live?

- Do you want to live in the same area or a different state?

- What style home will be practical to navigate?

- How much space do you need to be comfortable?

- What sacrifices are you willing to make?

- How much time and money can you commit to the moving process?

It’s also important to communicate early and often with your family.

If you’re married, discuss any concerns your spouse may have about the process.

Make sure your kids know what’s going on, too. Let them come over and help you sort through items, especially if they grew up in the house. This can prevent conflict and resentment down the road.

Financial Aspects of Downsizing

Saving money is one of the primary reasons people downsize in retirement. Cheaper housing is an easy way to boost your budget and increase your retirement savings.

- Increased Cash Flow

- Selling your home will likely result in a windfall of cash. This can boost your savings and grow your retirement nest egg.

- Cheaper Mortgage

- If your current home isn’t paid off, a new home with a lower monthly mortgage payment can give your budget room to breathe. The money you save each month can pay for a yearly vacation or finance a grandchild’s future education.

- Less Cleaning and Maintenance

- Americans aged 55 and older spend roughly $90 billion on home renovations each year — 47 percent of the national total. A newer home will likely need fewer repairs and have lower upkeep costs than an older home. And you probably won’t spend as much money hiring help to take care of the property.

- Lower Utility Bills

- Smaller spaces and fewer rooms mean lower utility costs. If you’re moving to a home with new windows or energy efficient appliances, you may save even more.

But before you make a move, get a handle on your finances. Hidden costs and poor planning can eat up potential savings if you’re not careful.

“Selling a home isn’t cheap,” Alan Caldwell, a financial advisor based in Nashville, told RetireGuide. “And you almost always spend more money when you move than you planned to.”

That’s why Caldwell, founder of On Track to Retire LLC, says it’s critical to get estimates from moving companies and set a budget in advance.

“During major life events like a move, we tend to think, ‘Well, I’m in a special time right now. It’s OK to spend money because I can control it later,’” Caldwell said. “But you need to be careful and track your spending as you go.”

- Homeowners Association Fees

- You’ll owe monthly fees if you move to a neighborhood, townhome or community with a homeowners association, or HOA. HOA fees vary widely, but some sources estimate costs between $100 and $700 per month. Fees are based on the services the HOA provides, such as lawn care. The more services and amenities, the higher the HOA fees.

- Getting Your House Market-Ready

- Staging is the process of preparing your home for sale in the real estate market. It can mean many things, from painting the walls and installing new flooring to landscaping improvements and replacing bathroom faucets. It’s not cheap, but it may be necessary if you don’t want your home to sit on the market forever. Add critical home repairs to your to-do list, too.

- Homeowners Insurance and Property Tax

- Just because you move to a smaller home doesn’t mean you’ll save money on homeowners insurance. Location also matters. External factors, including crime rates and proximity to natural hazards, can increase insurance premiums. Compare rates on the same coverage with different insurance companies to get the best deal. Be aware of changes to your property tax bill, too.

- Real Estate Agent Fees

- The standard commission for a real estate agent is about 6 percent of the home sale price. If you’re selling a $250,000 home, the buying and selling agents could take a total of $15,000. “That’s a ton of money,” Caldwell said. His advice? Be aware that closing costs and agent commissions will decrease your final payout.

- Purchasing Items for Your New Home

- After you downsize, you may still need to buy things for your new home. “We tend to spend a lot of time at Home Depot and Target when we first move,” Caldwell points out. Budget for these expenses before you move and only buy what you absolutely need.

Start Downsizing

You’ve decided to move. Now it’s time to start downsizing your current possessions.

But where do you start?

It isn’t a simple process. People have created entire careers out of helping others downsize for retirement.

It may seem daunting, but don’t let the task ahead overwhelm you.

“Decisions about what to keep and what to do with the rest can create decision paralysis,” Anna Novak, downsizing expert and owner of Simply Downsized LLC, told RetireGuide. “It’s a huge reason people have a hard time getting started.”

Novak and other experts recommend setting goals and timelines. Hold yourself accountable.

“Generally, once people know where they are going and can envision themselves there, they can start the process of letting go and get excited about a positive change,” Novak said.

Start Small, Give Yourself Time and Make a Plan

Rushing a move can amplify an already stressful experience.

Experts, like Novak, suggest starting small. Tackle one room before starting on another. Give yourself enough time to do the job right.

You won’t finish everything in one weekend. Most experts say the downsizing process takes at least six months to a year to complete.

So it’s helpful to put a plan in place.

You can find free detailed plans for two-year, one-year and six-month timelines on HomeTransitionPros.com.

The website also offers a 15-minutes-per-day plan along with a “Planning for Downsizing” workbook with checklists and activities to help you prepare.

Be Ruthless — and Realistic

It’s easy to fall in love with objects — and often very difficult to let them go.

“Downsizing involves letting go of 70 to 80 percent of the belongings it took you 20 to 30 years to accumulate,” Novak said.

Be realistic. Take a hard look at each item in your home. Identify the things that are most useful or loved. If you haven’t used something in more than a year, donate it or throw it away.

Downsizing involves letting go of 70 to 80 percent of the belongings it took you 20 to 30 years to accumulate.

Get in a habit of finding obvious things you can get rid of, such as duplicate household items, outdated paperwork, clothing that no longer fits and old magazines.

Document Your Current Space

It may be easier to let go of your home if you can remember how it once looked.

Take pictures of rooms in your house before you start downsizing. It can be comforting to look back at your old place or see the progress you’ve made getting it organized.

Measure the furniture you want to bring and write down the dimensions to ensure it will fit in your next place.

Document furniture arrangements and the placement of family photos on the walls. You can reference these later when you unpack in your new home.

Donate and Sell Items You Don’t Need

Selling unwanted items is a good way to raise extra money for your move.

It also helps to clear space, and there’s satisfaction in knowing that your old items will benefit others.

You can use websites like Craigslist or Facebook Marketplace to list belongings. You can also try apps like LetGo, OfferUp and NextDoor.com.

Make sure to accept only cash offers to avoid scams. You may also want to meet people at a public place for these transactions.

For smaller items, or those with lesser value, consider holding a yard sale. Other options include selling to collectors, used bookstores, online auction sites or music stores.

Return items to the people they belong to. Is your 40-year-old daughter’s prom dress still hanging in the closet? Ask her if she wants it. If she doesn’t, get rid of it.

Some charities, such as the Salvation Army, can pick up items from your doorstep free of charge.

Another option is a website called Give Back Box. Just pack your unwanted items in a box, go to the website and print out a free shipping label.

The box will then be mailed to a local charity. Give Back Box will even email you a receipt for a tax deduction.

Consider Hiring an Expert

A growing industry of professionals offers services to help retirees downsize.

Senior move managers specialize in helping older adults and their families with the emotional and physical aspects of relocation or aging in place.

They even have their own trade organization — the National Association of Senior Move Managers, or NASMM. Its membership has grown from 650 in 2012 to roughly 1,100 in 2020.

Similarly, professional organizers can help you declutter your home, offer emotional support, facilitate the disposal, donation or sale of unwanted belongings and set up systems that help you stay organized.

These professionals work alongside you. They do not provide cleaning services.

Costs can vary by state and job, but rates usually range between $75 and $150 an hour.

That may seem pricey, but the time and effort you save might be worth it.

“It’s like hiring a wedding planner for a wedding,” Mary Kay Buysse, executive director of NASMM, told RetireGuide. “Yes, you can probably do the job yourself. But if you want it done seamlessly and want less stress in your life, then hiring a professional is a smart move.”

Buysse said these professionals often offer a menu of services that can be tailored to fit your budget.

“It isn’t an elitist thing or something that only people with lots of money can afford,” Buysse said. “Sometimes families will only hire someone for part of the process.”

Home-service provider directories like TaskRabbit and Angie’s List are good places to find local help.

You can also use the NASMM’s online directory to find a senior move manager near you.

Cope with Your Emotions

Wading through a lifetime of memories is daunting — and draining.

Downsizing can uncover a well of emotions, including sadness, anxiety, stress and grief.

If something’s been a part of your home life for 40 years, it’s not easy to say goodbye.

According to a 2018 letter from the Harvard Medical School: “Understanding the triggers for these feelings and using strategies to navigate them may not change how you feel, but it may help the downsizing process go more smoothly so you can focus on your next chapter.”

If you find yourself in emotional turmoil, talk to someone. Invite a friend or family member over to help you sort through rooms.

Loved ones can listen to you reminisce about sentimental objects while providing you with a gentle push to let go of things you no longer need.

“If something’s been a part of your home life for 40 years, it’s not easy to say goodbye,” Buysse said. “Our items tend to become like members of the family.”

Even venting to an old friend over the phone after a stressful day of decluttering can calm your nerves and keep you focused.

If you don’t have someone to lean on, consider professional help. You may want to visit your primary care doctor or speak with a therapist.

Selling Your Current Home

Selling a home can be a time consuming, complex process.

But if you’re downsizing in retirement, it’s also important to understand taxes and how profits from your home sale can affect government benefits.

Beware of Capital Gains Tax

The Internal Revenue Service and several states levy capital gains tax on the difference between what you paid for your home — known as your cost basis — and what you sell it for.

The good news is that this probably won’t affect you. You can usually exclude up to $250,000 of capital gains on real estate if you’re single and $500,000 if you’re married and filing jointly.

So, if you first bought your house in the 1980s for $200,000 and you sell it today for $400,000, you won’t owe capital gains tax.

A few things may disqualify you from claiming that $250,000 or $500,000 exclusion. For example, the house must be your primary residence and you must have lived in it for at least two out of the last five years.

If capital gains tax is unavoidable, you may still qualify for a zero percent tax rate in 2021 if your income is less than $40,400 for a single person or $80,800 for a married couple filing jointly.

Otherwise, you may pay either a 15 percent or 20 percent tax rate. It depends on your filing status and income.

The Impact of Selling Your Home on Government Benefits

Owning a home won’t prevent you from collecting certain government assistance benefits, such as Medicaid or Social Security Income (SSI) disability.

But selling your home is a different story. This boosts your income, and the sudden cash may disqualify you from Medicaid and disability benefits.

For example, you must have less than $2,000 in countable assets to keep your Medicaid or disability coverage. Selling your home will net you more than $2,000.

To keep Medicaid, sale proceeds must be legally spent down or protected by the end of the following month.

With SSI, you have three months to buy a new home after selling your old one. If you do so and have less than $2,000 in your bank account, you will keep your SSI benefits.

If you don’t, you will lose your benefits for each month your assets exceed the permitted limit.

If it takes you more than 12 months to spend down money from your home sale, you may have to start the entire disability application process from the beginning.

And keep in mind that you’re not allowed to transfer money to a family member.

There are several legal ways to work around government benefit asset limits after selling a home. Consult a trusted legal professional for more information.

Moving Costs and Other Expenses

According to an October 2020 poll conducted for North American Van Lines, 45 percent of people who recently moved said the experience was the most stressful event in their lives.

One way to cut down on stress is by developing a solid moving plan that fits your budget.

- Cost to Rent a Moving Truck

- Renting a moving truck, such as a U-Haul, can cost between $90 for a small truck and a local move to $2,000 for a large truck and a long-distance move. The cost depends on how far you’re traveling, how much truck space you need, how long you keep the truck and gas.

- Cost to Hire a Moving Company

- Hiring a moving company to transport your belongings can cost between $80 to $100 per hour for short distances and $2,000 to $5,000 per load for long distances. Hiring a mover typically costs $25 to $50 per hour for each worker. The overall cost depends on the size of your home and the distance you’re traveling. Moving heavy objects or navigating staircases can cost extra.

- Full-Service Movers Cost

- According to HomeAdvisor.com, hiring a full-service moving company usually costs at least $2,300, but it depends on distance and the square footage of your current home. You may be able to spend as little as $900 for a local move, or as much as $10,000 for a cross-country move. Make sure to get visual estimates and total cost estimates. Understand the difference between binding and nonbinding estimates to avoid expensive surprises.

- Cost to Rent a Moving Container

- Renting a moving container can cost an average of $3,000 a month, according to Move.org. Moving containers cost an average of $2.50 per mile to transport. But the total price may be as low as $250 for a small container and a local move to $4,000 for a large container and a cross-country move. You can request a moving container from companies such as PODS and U-Pack. They drop off the container, and you load your belongings into it on your own time. The container company will then pick it up and drop it off at your new location. If you’re downsizing, you may also consider renting a storage unit.

This can allow you to keep items that are too difficult to part with.

- Memorabilia

- Boxes of old family photos and letters

- Oversized items

- Antique furniture or family heirlooms

According to Zillow, the average national cost of a storage unit ranges from about $50 per month for a small unit to $300 or $400 for larger units.

If your main reason for downsizing is to cut costs, you need to be mindful of this added reoccurring expense.

Expert Tips on Downsizing for Retirement

Vickie Dellaquila is a Pittsburg-based professional organizer with nearly two decades of experience. She is the owner and founder of Organization Rules, Inc. and has given presentations at several national conferences and conventions. She is also the author of the book, “Don't Toss My Memories in the Trash: A Step-by-Step Guide to Helping Seniors Downsize, Organize, and Move."

Downsizing is extremely emotional and physical work. You’re going through a lifetime of memories. It’s exhausting. Let yourself experience those emotions, whether you want to cry, laugh or be angry. Giving yourself enough time will also help you process those feelings.

You’ve spent a lifetime accumulating stuff. It’s going to take time to go through it all. I always tell people to start now. You may be able to do it in a month, but I tell people to give themselves at least six months. A year or two years is even better.

When you start the process, put a downsizing session on your calendar, the way you would a doctor’s appointment. So, from 9 a.m. to noon on Saturday, I’m going to work on the kitchen. Stick to it. Try to avoid procrastination.

Start with areas you don’t really live in, like spare bedrooms, the basement or the attic. Many times, these spaces have lots of things you aren’t using, or that you forgot you had. The garage is another good place to start because this is usually an exit route. It can be physically easier to move things out of this space.

If you know where you’re moving, getting a floor plan will certainly help you make decisions. It can also help you figure out where everything will go and how much space you really have.

Finding a New Home

When you’re looking for a new residence, take time to consider your needs. Make sure the space fits your lifestyle, budget and level of independence.

You may decide to purchase a new home, move in with family, transition to an assisted living facility or rent a townhouse or condo.

A great freedom in retirement is the chance to live where you choose. You may have bought your former home because it was in a good school district or close to work. Your life is different now, so explore your options.

Look for housing that puts you closer to things you care about, like your family, an airport, public transportation, a grocery store or your favorite nature preserve.

It’s also critical to be realistic about what your physical limitations will be in the future. For example, a one-floor house will be easier to navigate than a two-story house.

Downsizing Without Moving

Moving to a new location isn’t right for everyone. Some people want to stay in their home but still want greater financial independence.

There are a few options if you’re interested in downsizing without moving.

- Rent Out a Room

- Renting a room in your home, or even converting the property to dual occupancy can increase your monthly income. But be careful and selective with potential renters. Speak with a legal advisor who can help you draft a simple lease agreement for your new tenant. Research your rights as a landlord. Lay out clear ground rules and restrictions before you let someone move in.

- Consider a Reverse Mortgage

- Some seniors opt for a reverse mortgage to boost income and age in place. A reverse mortgage allows people aged 62 or older to stay in their homes while drawing on the equity they've already built. But there’s risk involved and a long-term financial impact, so make sure to get independent financial advice first.

- Pretend You’re Moving and Declutter Accordingly

- It’s always a good idea to declutter and organize your space — even if you’re not going anywhere. Selling unwanted or unused items can also raise money you can reinvest in home repairs or save for the future.

Downsizing for retirement means something different to everyone. It’s often stressful and requires careful planning and financial considerations.

But it can also be a rejuvenating experience. Focus on the positive aspects of the transition, and work toward making your new space feel like home.

Additional Resources

- Donation Town

- Don’t want the hassle of transporting big objects to your local thrift store? There are dozens of charities that can send a truck to your home and pick up your belongings for free. Enter your zip code into the Donation Town pickup service directory to find nonprofit organizations that offer this service.

- National Association of Productivity & Organizing Professionals

- If you want to hire a professional organizer to help you declutter your home, the National Association of Productivity & Organizing Professionals can help. Enter your zip code into the organization’s directory, and you’ll find numerous professional organizers and productivity consultants near you.

- National Estate Sales Association

- This website offers multiple guides about estate sales and how to sell personal property.

- To view the original version of this article visit www.retireguide.com/guides/downsizing-for-retirement/

- Seniors Blue Book was not involved in the creation of this content.

Other Articles You May Like

Lower Your Blood Pressure Using These 9 Effective Methods

It takes more than prescription medication to lower or control blood pressure, although they play a vital role in treatment. Other dietary and lifestyle changes can be instrumental in maintaining a healthy blood pressure. Before your doctor increases your medication dosage or adds another prescription to your treatment, he might recommend other changes in your eating habits or lifestyle, such as limiting sugar and alcohol, increasing exercise, and getting better sleep.All of these and more can help set you up for success for lowering blood pressure, especially as you age. High blood pressure, also known as hypertension, often has no recognizable symptoms but is a major risk factor for heart disease and stroke.Most healthy adults should aim for a blood pressure reading below 120/80 mm Hg. Your blood pressure is considered high at 130/80 or above. Anything in between these ranges is considered elevated blood pressure and means you are at risk for developing high blood pressure. But this isnt inevitable.Here are 9 effective methods to lower your blood pressure.1. Get Adequate ExerciseExercise is a key ingredient for lowering blood pressure and can help you manage it long term. According to research, both aerobic and resistance training positively affect blood pressure and can even lower it for up to 24 hours after exercising.The key is to get regular exercise, meaning that its part of your daily routine. Its about regularly increasing your heart rate and breathing so that over time your heart is strengthened. A stronger heart pumps with less effort, putting less pressure on your arteries. This means lower blood pressure.So how much exercise is required to affect cardiovascular health? You should aim for 30 minutes per day, five days per week. Thats 150 minutes of moderate-intensity exercise weekly. Moderate intensity exercise is defined by your heart rate during a work out. Anything below this range is too low to benefit cardiovascular health and anything above it is unnecessary. If you are exercising for health, these are the target heart rate ranges.Age (years)Target Heart Rate Range (beats/min)5085-1195583-1166080-1126578-109Other than intentional exercise, you can also increase activity by doing the following:Using the stairsWalking instead of drivingWorking around the houseGardeningBike ridingPlaying a sportBut be sure to clear any new exercise routine with your doctor to be sure you are healthy enough for moderate-intensity workouts.2. Manage Your WeightExtra body weight strains your heart and cardiovascular system, because it makes them work harder. This creates more pressure inside your arteries and can raise blood pressure. If youre overweight with a body mass index (BMI) over 25, it can help to lose 5-10 pounds. Losing weight may lower your blood pressure and your risk for other health problems.There are three major components to lowering BMI:Be more physically activeEat lessEat a healthy diet3. Eat Less Sugar and Refined CarbsCutting back on sugar and refined carbs can help you lose weight while lowering blood pressure. One study found that people who are overweight or obese who followed a low carb and low fat diet dropped their diastolic blood pressure (bottom number) by about 5 points and their systolic pressure (top number) by about 3 points after just six months.You can start by replacing some of the refined carbs with more whole grain varieties and foods that are less processed. Be sure to read labels and notice the sugar content in common foods you eat. Its often best to eat fewer prepackaged foods as these often contain more simple carbs and sugars.Instead, snack on produce and include more lean protein in your diet.4. Eat More Potassium and Less SaltEating a diet high in salt can increase your risk for high blood pressure. But if you eat more potassium and cut back on salt, you can lower your blood pressure. Science hasnt determined why salt impacts blood pressure, but its believed to have something to do with water retention and inflammation in blood vessels could be factors.Potassium helps your body eradicate salt and even relieves some of the pressure in your blood vessels. Think of it as a counterbalance to salt and its effects. Cutting back on salt and adding more potassium to your diet can notably lower blood pressure over time.High potassium foods to incorporate into your diet:Dried fruit (apricots, prunes)Milk and yogurtLentils and kidney beansVegetables like tomatoes, potatoes, and spinachFruit like watermelon and bananasIf you have kidney disease, talk with your doctor before increasing potassium in your diet, as it could be harmful.5. Manage StressManaging stress benefits your overall health and positively affects your blood pressure. Stress has a direct impact on your body and its systems. Its important that you learn to recognize the symptoms of stress and its triggers. Its best to eliminate sources of stress when possible. But much of what causes your stress probably cant be set aside. In this case, youll need to learn to manage stress in a healthy way.Consider some of these methods and determine what works best for you:Taking a walk (or getting exercise)Reading a bookPracticing deep breathingListening to musicMeditation or prayerThese are ways you can decompress from daily stress and set your mind elsewhere. This type of relief can relax your body and keep your blood pressure from rising. Chronic stress, especially when poorly managed, keeps your body in an anxious state with an elevated heart rate and increased blood pressure.6. Get Plenty of Quality SleepWhen youre sleep deprived youre at greater risk for high blood pressure. Blood pressure often lowers a bit while sleeping, giving your system a rest. But if you havent slept well or enough, your body doesnt get this needed break. And without it, pressure continues to build. If you do this night after night, it can have long-term effects on your blood pressure.Here are some tips for getting better sleep:Keep a regular sleep scheduleExercise (but not too close to bed time)Leave devices outside your bedroomSleep in a cool, dark roomAvoid caffeine and alcohol too close to bedtime7. Limit Processed FoodsA strict definition of processed foods is any food that has been changed from its natural state. Technically, just cutting and washing a food is a change to its natural state, and so not all processed food is bad. But often, when this phrase is used, its referring to overly processed foods that make them less healthy. This type of processed, pre-packaged food often includes additives like preservatives, sugars, fats, and not-so-natural ingredients.Bad processed foods include ingredients you dont want that can also increase blood pressure and negatively affect your health. They often contain higher levels of sodium, sugar, saturated fat, and inflammatory chemical ingredients.Common examples include:Processed meats (lunch meats, sausage, ham, etc.)Fried foods or fast foodProcessed snacks (chips, crackers, cookies, etc.)And be careful about foods labeled low fat since they often include more sugar or salt to compensate for the lower fat content. They may be lower in fat but arent necessarily healthy overall.8. Try SupplementsYou can try supplements to help manage blood pressure. Some widely used options include:Omega-3 fatty acids or fish oilWhey proteinPotassiumMagnesiumWhile you may see some benefits from supplement use, there is not enough scientific evidence to verify that most of them can decrease blood pressure.Be sure to check with your doctor before using any supplement as some conditions and medications might cause complications.9. Limit AlcoholAccording to research, your heart rate can increase for up to 24 hours after drinking just an ounce of alcohol. It appears that blood pressure drops for the first 12 hours but then increases. The average alcoholic beverage contains about half an ounce of alcohol.And dont be fooled by red wine. While the idea that its heart healthy has been widely spread, the America Heart Association warns that too much can be harmful. Instead, limit your alcohol consumption, even red wine, to two standard drinks per day for men and one drink per day for women, if you drink at all.One drink or serving of alcohol is considered to be:One 12-ounce beer4 ounces of wine1.5 ounces of 80-proof spirits1 ounce of 100-proof spiritsConsidering general health and common medication interactions, it may be best to skip the alcohol completely.Blood Pressure Management Is KeyManaging your blood pressure as you age is a critical component of aging well. While you can try supplements and take medications when needed, these alone wont necessarily prevent high blood pressure. If you want to prevent additional or stronger medications, or hope to avoid prescriptions altogether, then be sure to get daily exercise, sleep well, manage stress, and limit salt and sugars. Your diet and lifestyle are keys to lower blood pressure.TYE Medical offers premium incontinence products in a variety of sizes and absorbency levels. Get free and discreet shipping when you shop our online store.

Breast Cancer: What You Need to Know

Breast cancer is the most common type of cancer among women in the U.S. besides skin cancers. Each year, about 30% of new cancer diagnoses in women are breast cancer. No one wants to hear the word cancer or spend time researching their diagnosis online. Cancer of any type is a scary thing.But there isnt just one type of breast cancer. It can develop in different types of breast tissue and spread throughout the breast and beyond. Like other cancers, your diagnosis is labeled with a stage of cancer, usually levels one through four, with four being most severe. Regular breast cancer screenings allow your doctor to catch a tumor in its earliest stage, increasing your chances for successful treatment.This guide provides information on breast cancer from early symptoms to types of treatment to help you feel more prepared and informed as you take on this battle against cancer.What Is Breast Cancer?This might seem like a very basic question, but there is more to it than you think. Breast cancer means there is a malignant tumor somewhere in your breast, and the details will determine the type and severity of cancer.A malignant tumor means that cells have clustered together, forming a mass that grows out of control. These can move or metastasize to surrounding tissues or other body parts. Breast cancer can form in any of your three breast tissues, which are:Lobules (milk-producing glands)Ducts (what milk travels through)Connective tissue (surrounds lobules and ducts)Cancer most often begins in the lobules or ducts but can start in the surrounding connective tissue. Its categorized as either invasive or noninvasive. Invasive breast cancer spreads or invades other tissues, while the noninvasive type remains in the breast lobule or duct.Symptoms and Signs of Breast CancerWhen you notice any of these symptoms, make an appointment with your doctor as soon as possible:A lump in or near your breast or armpit areaWarm or tender breastA hard or swollen area in your breastUnexplained changes in the texture, size, color, or shape of your breast or nippleSkin dimples or enlarged pores on your breastRedness, swelling, scaliness or pain in your breast or nipplesNipples turn inward for no apparent reasonIrritated or itchy breastA rash on your breast (a sign of inflammatory breast cancer) tendernessIf you notice a lump, dont assume the worst. Almost 80% of all breast lumps are non-cancerous or benign. Common causes of benign lumps include:CystsChanges in the fibrous tissue due to hormonesFatty tissue due to breast traumaIntraductal "papilloma" or wart-like growthsFibroadenomas or solid breast lumpRegardless of the type of lump you feel, you should see your doctor for a thorough evaluation to rule out a malignant breast tumor.Breast Cancer Risk FactorsNaturally, being a woman increases your risk of breast cancer. Other risk factors include:Over 50 years of ageA family history of breast cancerGeneticsPrevious radiation exposureWomen can develop breast cancer before age 50, but its less common. If youre concerned about your breast cancer risk, your doctor can help you assess your specific risk and guide you through extra precautions or screening if necessary.Diagnosing Breast CancerThe most common type of breast cancer screening is a mammogram, which is an x-ray that uses low-dose radiation. This allows your doctor to see abnormalities in your breast tissue.If your mammogram reveals something suspicious, your doctor will likely order an MRI (magnetic resonance imaging), ultrasound, or a 3D mammography to get a better look at the abnormality. This type of imaging allows doctors to see breast tissue in greater detail.Stages of Breast CancerStages describe how the cancer has grown or spread, making them stages that describe the advancement of the cancer. Stages are typically indicated by Roman numerals and have subcategories of A, B, C or D.Stage 0: Noninvasive cancer with no evidence of leaving the area of breast it started in.Stage 1: Cancer cells are actively spreading to breast tissue surrounding the origin of the cancer. But the tumor (group of cancer cells) is still very small and easily treated.Stage 2: The cancer is invasive and growing but is confined to the breast or close lymph nodes. It is usually still treatable.Stage 3: The cancer is no longer confined to the breast and nearby lymph nodes. It has begun invading other lymph nodes, muscles, or other tissues surrounding the breast.Stage 4: The cancer is advanced and has spread to several organs or body parts. Stage 4 breast cancer is usually incurable, but you can live for several more years with treatments.Types of Breast CancerNon-Invasive Breast Cancer: DCIS and LCISThese are non-invasive cancers that remain contained within the tissue where it began and are therefore called carcinoma in situ. There are two types: ductal carcinoma in situ (DCIS) and lobular carcinoma in situ (LCIS). These breast cancers are usually discovered after imaging and often dont cause symptoms.DCIS is found in the lining of your milk ducts and has not yet spread to other tissues. But if not treated, it can invade other tissues and become more serious. Likewise, LCIS is non-invasive and is found in the lobules of your breast where milk is produced. This is usually considered pre-cancer and is less common than DCIS but is more likely to become invasive if it develops into cancer.Invasive Breast Cancer: IDCThe most common type of breast cancer is invasive ductal carcinoma (IDC). It accounts for 80% of all new breast cancer diagnoses and is the type of breast cancer most likely to develop in men.IDC begins in your milk ducts, like DCIS, but it doesnt remain contained and spreads outside the duct and into surrounding tissues, even invading your bloodstream and lymph nodes.Treatment usually involves a combination of radiation, surgery, chemotherapy, hormone therapy, targeted therapy, and immunotherapy. But the approach will depend on the specific type of breast cancer you have and its characteristics like the degree of aggressiveness. Some breast cancers lack receptors that will respond to the usual medications. This is called triple negative or HER-2 negative breast cancer. Your doctor will work to create a specialized treatment tailored to the weakness of your tumor type.Breast Cancer OutlookYour prognosis will depend upon how healthy you are and the stage of breast cancer youre in. However, its encouraging that the death rate from breast cancer has been dropping. Most women survive this type of cancer, and 90% of women will live at least five years after their diagnosis.Breast cancer can be recurrent, meaning that it returns after your initial treatment. This recurrence can happen months or years after seemingly successful treatment. The highest risk for recurrence is within the first two years after completing your treatment. However, most breast cancer survivors wont have a recurrence.Metastatic or stage 4 breast cancer that has spread to other parts of your body is not currently curable. But with the right treatments to control its growth and spread, you can continue living a fulfilling life for years to come.Breast Cancer Treatment OptionsYour doctors will evaluate the stage and aggressiveness of your tumors. Most often, surgery is the prescribed treatment, along with secondary treatments to ensure that post-surgery cancer cells dont survive.Surgical options include a lumpectomy or mastectomy.A lumpectomy means that a small portion of the breast encasing the tumor is removed. If your surgeon must remove more of the surrounding tissue, it is considered a partial mastectomy.A mastectomy means that one or both breasts are removed. Sometimes lymph nodes and armpit tissue are removed also.Radiation and chemotherapy are accompanying treatments that are often used post-surgery to kill any possible cancer cells that are left behind. Your doctor will recommend which treatment is best for you based on your tumor and the likelihood of cancer cells spreading.Other treatments include medications like hormone therapy and biologic targeted therapy.How to Prevent Breast CancerOf course, you cant change all your risk factors like age and family history. But you can adjust some aspects of your lifestyle to stay healthy overall and decrease your risk of breast cancer.Try making these lifestyle modifications:Dont drink more than one alcoholic beverage per day.Dont smoke.Maintain a healthy weight.Breastfeed your baby for at least several months.Choose non-hormonal treatments for menopause symptoms.Avoid radiation exposure (get medical imaging only when necessary)The Battle with Breast CancerBreast cancer can be complex, especially if not diagnosed in its earliest stages. Regular preventative screenings like self-exams and mammograms are necessary for early detection. Most breast cancer will spread if not treated in a timely fashion. Surgery is the most common treatment method and may be accompanied by radiation or chemotherapy. If you notice and change the appearance or feel of your breasts, contact be sure to get in touch with your physician. You can reduce the risk of developing breast cancer when you limit alcohol, radiation exposure, and maintain a healthy weight.

Why You Should Watch Your Diet During Menopause

Hormones become a focal point for women in mid-life as they move women into the transitory phase of menopause. These chemical messengers influence numerous processes of your body, which means theyre necessary to keep your systems functioning properly. This is why you may feel physically unwell or mentally off during this time of life. But you can find ways to bring your hormone levels into balance, helping your body to maintain wellbeing and proper function. Your diet can play a key role in achieving this goal.Diet Affects Estrogen LevelsSince foods dont contain estrogen, your diet has more of an indirect influence on your hormones, affecting fluctuations in your hormones. Youll notice these fluctuations most during the earliest stage of menopause, known as perimenopause. Dips and spikes in estrogen are frequent during perimenopause but tend to even out as they move closer to the final phase of menopause and the cessation of your cycle. When estrogen levels drop, you may experience night sweats, hot flashes, and changes in mood. However, eating foods containing phytoestrogens (estrogen-like compounds) may help regulate menopause symptoms. They mimic estrogen in the body. Found in plant foods, phytoestrogens are consumed when you eat seeds and soybeans. But the effects on estrogen are mild, and they may only slightly raise estrogen levels, specifically when you consume isoflavones.The research on phytoestrogens and their impact on estrogen is mixed and more studies are required. More research is necessary to determine whether certain foods or nutrients may help raise estrogen levels during menopause. Foods that May Lower Estrogen If your menopause symptoms are due to lower estrogen levels, then eating a diet rich in fiber may help to bring your body into balance. High fiber foods include fruits, vegetables, and whole grains like oats, quinoa, and brown rice. Eating more of these may reduce estrogen levels, but this doesnt mean you should avoid these foods if your estrogen is too low. They have too many other health benefits to eliminate them from your diet. The better option is to seek other ways to raise your estrogen levels.Diet and Estrogen TakeawaysIts generally good for your health to eat foods rich in phytoestrogens, especially isoflavones. You can positively impact blood cholesterol levels and reduce your heart disease risk when you include more soy and flaxseed in your diet. You might also experience other benefits like improved menopause symptomsA higher fiber diet also improves blood sugar levels and digestion and can have the added benefit of regulating hormones during menopause.Diet Affects InsulinIts not only female hormones that affect menopause. Insulin and glucagon also play a notable role in hormone regulation during this period of life. Diet has a more direct impact on insulin hormone. In other words, what you eat more directly impacts insulin than estrogen.However, its also true that hormone changes during menopause affect your glucose levels. These hormone fluctuations make women more insulin resistant, which means that your body is not as able to process sugars efficiently and sugar in the bloodstream is not used effectively. This leads to high levels of blood sugar that over time leads to diabetes that if left unchecked, will damage organs and body parts.Menopause and InsulinIf you eat too much sugar or two many simple carbohydrates that quickly break down into sugar during digestion, you will experience spikes in blood sugar as your system is overwhelmed and not able to process the incoming sugars quickly enough.Since hormonal changes in women during menopause already make them less equipped to properly process carbohydrates and sugars, its best to make some adjustments.Diet and Insulin TakeawaysDuring menopause choose foods that release sugar into your bloodstream more slowly. Good helpful choices include:VegetablesBeansLentilsOatsBranWhole grain breads Avoid or limit simple or refined carbohydrates which will spike your blood sugar. These consist of anything made with white flour or sugars (white or brown).Diet Affects Cortisol LevelsCortisol, known as the major stress hormone and is secreted by your adrenal glands. Due to hormonal changes during menopause, your body is already susceptible to weight gain, anxiety, and hot flashes, symptoms which high cortisol levels can worsen. During this time, its best to avoid alcohol and caffeine, which can boost cortisol levels and make menopause symptoms worse.While cortisol is an essential hormone responsible for the flight-or-fight response, when it remains chronically high, it causes a number of health concerns, such as:High blood pressureCognitive declineBone lossSleep disruptionsHeart diseaseIncreased body fatDiet and Cortisol TakeawaysAvoid alcohol and caffeine during menopause to help keep your hormones balanced and minimize menopause symptoms. You may find that nixing alcohol and caffeine reduces hot flashes and weight gain.Diet and Menopause: What to RememberA healthy diet that includes soy, flaxseed, and plenty of fiber can go a long way toward keeping your hormones balanced during menopause. While adding these foods to your diet can be helpful, its also important to avoid simple carbs, alcohol, and caffeine which can knock your hormones out of balance, not only increasing menopause symptoms but also negatively impacting your health. TYE Medical offers premium incontinence products in a variety of styles and absorbency levels. Shop our online store for free and discreet shipping on all orders.

Local Services By This Author

Alder Terrace Gardens

Assisted Living 26563 Sandhill Blvd., Punta Gorda, Florida, 33983Alder Terrace Gardens is a welcoming and nurturing environment for seniors who value their independence but may need some assistance with daily activities. The focus on creating a home-like atmosphere is wonderful, as it helps residents feel comfortable and at ease in their surroundings. Providing home-cooked meals adds an extra touch of warmth and familiarity, while the weekly entertainment and Wellness and Mobility Center offer opportunities for socialization and physical well-being. It's clear that Alder Terrace Gardens is committed to not only meeting the needs of their residents but also enriching their lives with meaningful experiences and a strong sense of community. The location amidst serene surroundings offers a peaceful environment conducive to well-being. The variety of room options ensures that residents can find the accommodation that suits their preferences and needs.The provision of three chef-prepared meals a day, along with snacks and catered holiday events, reflects a commitment to providing nutritious and enjoyable dining experiences. The on-site Wellness & Mobility center further enhances residents' quality of life by focusing on preventative strength building, stretching, and appropriate exercise. This personalized approach to fitness promotes overall health and vitality.Most importantly, the promise to exceed expectations and prioritize the well-being of residents underscores the dedication of Alder Terrace Gardens to providing exceptional care and support. Families can trust that their loved ones will be nurtured and cherished in this welcoming community.