The 2021 Part D Senior Savings Model

AIS Medicare & More

May 12, 2021

Colorado - Western Slope

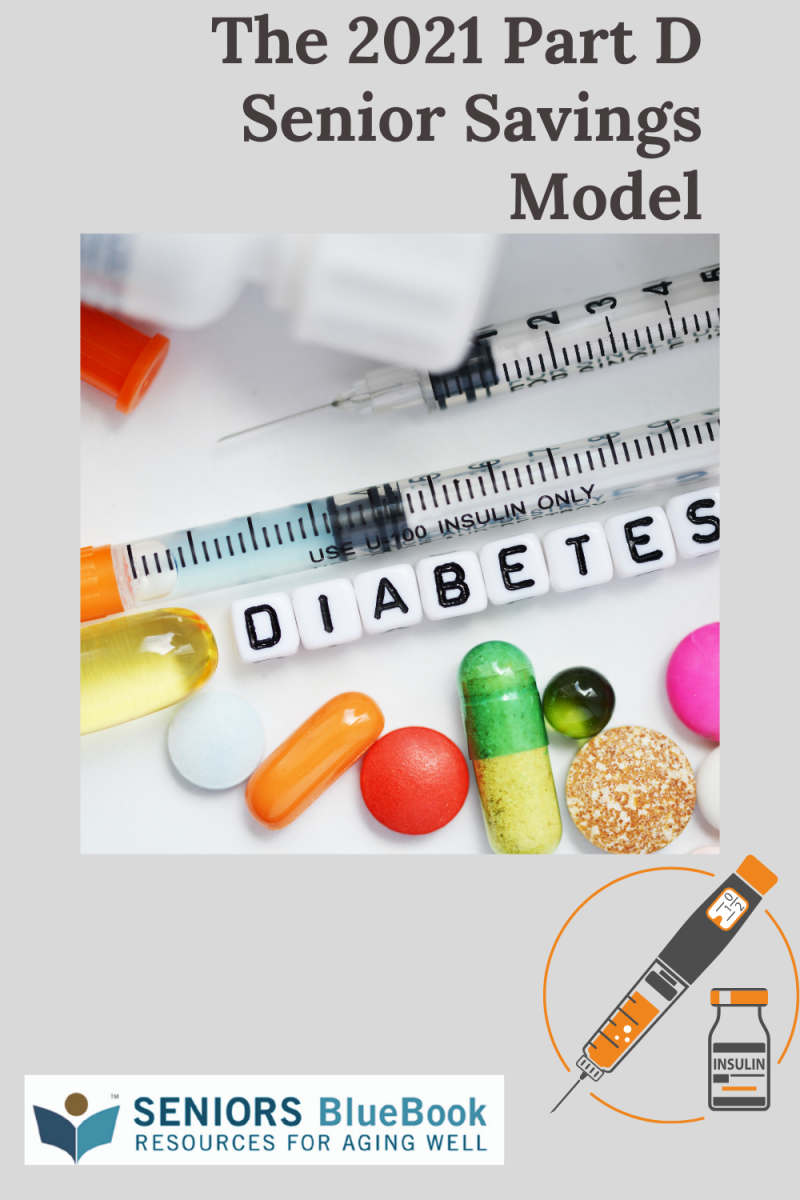

For diabetics, access to insulin is a critical component of their medical care. Failing to effectively manage diabetes results in increased risk of serious complications, ranging from vision loss to kidney failure to foot ulcers, amputations and heart attacks. Unfortunately, for many seniors the cost of insulin is a barrier to appropriate medical management of diabetes.

CMS Part D Senior Saving Model is designed to address President Donald Trump's administration promise to lower the prescription drug costs and provide Medicare patients with new choices of Part D plans that offer insulin at an affordable and predictable cost where a month supply of plan-formulary insulin costs to $35 each.

Lower Medicare Part D costs for Insulin

Medicare Insulin Coverage Program Details - Senior Savings Model

The new Senior Savings Program allows for Medicare Part D sponsors to offer a Part D benefit design that includes predictable copays in the deductible, initialcoverage, and coverage gap phases by offering supplemental benefits that apply after manufactures provide a discounted price for broad range of insulins included in the program.

The Senior Savings Model aims to reduce Medicare expenditures while enhancing the quality of care for seniors, and to provide beneficiaries with additional Medicare Part D Plan choices. There are participating stand alone Prescription Drug Plans and Medicare Advantage Prescription Drug Plans.

Beginning January 1, 2021, Medicare Part D sponsors that participate in the program will offer beneficiaries Prescription Drug Plans that provide supplemental benefits for insulin coverage in the coverage gap phase of the Medicare Part D benefit. Participating pharmaceutical manufactures will pay the 70% discount in the coverage gap for the insulins that are included in the program (click image above to see which insulin drugs are covered in the new Medicare Insulin Program), but those manufacturer discount payments would now be calculated before the application of supplemental benefits under the program.

As a result of the new program, seniors who take insulin and enroll in a plan that is participating in the Seniors Savings Model would now be saving on average $446, in annual Out-Of-Pocket costs of insulin, which is savings of about 66%. This predictable copay will provide improved access and affordability of insulin.

Participating Pharmaceutical Manufactures

Eligible Pharmaceutical manufactures had the opportunity to volunteer to participate in the Senior Savings Model. The following Pharmaceutical Manufactures are participatingin the Medicare Part D Senior Savings Program in 2021:

Eli Lilly and Company

Novo Nordisk, Inc.

Novo Nordisk Pharma, Inc.

Sanofi-Aventis U.S. LLC

Across the nation, 1,635 Prescription Drug Plans, including both Medicare Advantage Prescription Drug Plans and Stand alone Prescription Drug Plans are participating in the Senior Savings Model for 2021. This covers an estimated 13.2 million enrollees. Seniors who use insulin in all 50 States, D.C., and Puerto Rico will have a choice of a Medicare Part D Senior Savings Model participating plan in their area.

Other Articles You May Like

Post-Hospital Home Care Are Essential for Recovery

Why After-Hospital Care at Home is Key to a Safe & Speedy Recovery for Grand Junction, Colorado SeniorsRecovering after a hospital stay? Learn how post-hospital home care supports a safe, smooth recovery, reduces complications, and prevents readmission. Discover the benefits of after-hospital care at home. Leaving the hospital is a significant step in your recovery, but the healing process doesnt stop there. Proper after-hospital care at home is essential for a smooth recovery, reducing the risk of complications and hospital readmission. In fact, research indicates that people receiving home healthcare services have a considerably lower risk of being readmitted to the hospital within 30 days compared to those who do not receive such care; this reduction can be as high as 60% in some studies. Keep reading to discover why post-hospital home care is crucial and how it can support a faster, safer return to daily life for seniors and other adults in Grand Junction and the surrounding Colorado communities.What is Post Hospital Care in Grand Junction?After-hospital carealso known as post-hospital care, transitional care, in-home recovery care, or post-hospital home carerefers to the support seniors and other adults need after being discharged from the hospital to ensure a safe and smooth recovery at home.After surgery or a hospital stay, many individuals prefer to recover at home, where they feel most comfortable. However, since they are still in the healing process, its essential to follow their doctors recommendations closely to regain strength. Depending on their condition, they may need additional support for a short period or several months.Every situation is different, which means that every person's in-home recovery care needs will be different. Transitional care services can include a wide variety of services, such as:Assistance with implementing the patients recovery planCoordination with medical staffMedication remindersPersonal careCompanionshipTransportationLight HousekeepingRespiteFamily members often step in to help with in-home recovery care, and in some cases, their support may be enough. However, professional transitional care is often necessary to ensure a safe and smooth recovery. If loved ones lack the time, skills, or energy to provide proper care, hiring an in-home recovery professional can be the best way to promote healing, prevent complications, and support a faster return to daily life.The Benefits of Post-Hospital Home Care in Grand JunctionPost-hospital home care doesnt just make a patients life easier; it has been scientifically proven to improve recovery outcomes. The benefits of post-hospital home care include:Comfort of home. Most people prefer to recover in the comfort of their own home, surrounded by loved ones in a familiar setting. A 2018 study published in the New England Journal of Medicine found that people who received in-home recovery care experienced significantly less stress than those who remained in the hospital for an extended period.Personalization. Everyone has unique needs after a hospital stay, and at-home care allows for greater personalization than hospital-based recovery. Unlike hospitals, transitional care services are not restricted by schedules, staffing, or resource limitations. This flexibility enables patients to receive fully customized care tailored to their routines, preferences, and recovery plans.Safety. Recovery is a critical phase of healing, and post-hospital home care significantly improves the chances of a safe and smooth recovery. In-home care ensures that patients receive the supervision needed to follow their doctors recovery plan while reducing risks such as falls, infections, and medication errors. Transitional care professionals can provide medication reminders, assist with hygiene, and support daily living activities to enhance safety.Independence. Recovering at home empowers seniors and other adults to take an active role in their healing process. With support from a family member or professional caregiver, patients maintain more control over their daily lives. As their health improves, they can gradually resume more tasks on their own, fostering a sense of independence and autonomy.Community. Hospital stays can feel isolating, but at-home recovery allows patients to stay connected with friends and family. Without hospital visitation restrictions, loved ones can visit freely, and with transportation assistance, patients can continue participating in social activities aligned with their recovery plan.Cost-effectiveness. Hospital bills add up quickly, especially for extended stays. In contrast, post-hospital home care is significantly more affordable while providing greater comfort. Hiring a professional for transitional care services costs only a fraction of what a prolonged hospital stay would.Improved recovery outcomes. The greatest advantage of post-hospital home care is improved recovery. A 2021 study published in the Journal of the American Medical Association (JAMA) found that in-home recovery care not only speeds up healing but also lowers the risk of infection. Additionally, the AMA found that patients receiving post-hospital care at home are 44% less likely to be readmitted to the hospital.Simply put, in-home post-hospital care is often the best choice following a surgery or illness, and professional transitional care services can help your family make sure your loved ones needs are met. How to Prepare for After Hospital Care at HomeBefore beginning after hospital care at home, you should make a few simple preparations for yourself or your loved one.Follow these steps to build the proper infrastructure for in-home recovery care:Consult with the patients doctor about their recovery plan.Make plans for the patients transportation from the hospital to home.Clean and organize the home.Purchase and set up any necessary equipment, like shower railings.Consider the patients nutrition needs and dietary restrictions and plan meals accordingly.Prepare a schedule for any prescribed medications.Address any limitations to mobility or daily living activities. Consider hiring an in-home post-hospital care agency, like the friendly, knowledgeable team at Comfort Keepers.Enjoy a Smooth, Safe Recovery with Comfort Keepers Grand JunctionComfort Keepers Grand Junction is a post-hospital home care provider in Colorados Western Slope. Our transitional care services are designed to provide patients with the support they need to get back on their feet as soon as possible.Our agency provides in-home senior care services to seniors and other adults in Grand Junction, Redlands, Clifton, Fruita, Palisade, Whitewater, Gateway, Orchard Mesa, Appleton, Loma, Glade Park, Fruitville, Glenwood Springs, Battlement Mesa, Parachute, and Rifle, Colorado. When you choose Comfort Keepers Grand Junction, you and your loved ones can benefit from:Experienced, compassionate caregiversPersonalized recovery plansEnhanced home safetyHelp with transportation, light housekeeping, and errandsMedication remindersAssistance with daily living activities, like bathing, dressing, and mobilityPeace of mind knowing that your loved ones are taken care of by professionalsAt Comfort Keepers, our clients are more than just clients; they are family. We care for the seniors in Mesa, Delta, Montrose, Ouray, and Garfield counties like they are our own loved ones, incorporating time-tested best practices alongside cutting-edge techniques.Contact Comfort Keepers Grand Junction today to learn how our post-hospital home care services in Mesa, Delta, Montrose, Ouray, and Garfield counties can support a safe, smooth recovery call today to ask how, 970-241-8818.

9 Signs of Caregiver Burnout & How Respite Care Can Help

Feeling overwhelmed as a family caregiver? Learn the 9 warning signs of burnout and how Comfort Keepers' respite care in Delta, CO, can help you rest and recharge.Caring for an aging loved one is one of the most selfless and rewarding things you can do. In fact, 43.5 million Americans serve as unpaid family caregivers, ensuring their loved ones receive the support and care they need at home. However, caregiving is also physically, emotionally, and mentally demanding. Even the most devoted caregivers need time to rest and recharge.If youre feeling drained, overwhelmed, or stretched too thin, it may be time to consider respite care. This article will guide you through what respite care is, when to consider it, and the key signs of caregiver burnout that indicate its time for a break.What is Respite Care for Family Caregivers in Delta, CO?Respite care is a temporary caregiving service designed to provide relief for family caregivers while ensuring their loved ones continue to receive high-quality care. It allows you to step back, focus on your well-being, and take care of personal responsibilities without disrupting your loved ones routine.Respite care services include:Meal Preparation Ensuring your loved one has nutritious meals and snacks.Transportation Helping with doctors appointments, errands, or social visits.Household Support Light housekeeping, laundry, and organization.Personal Care Assistance Help with bathing, dressing, and hygiene.Companionship Providing meaningful social interaction to keep your loved one engaged.By incorporating respite care into your routine, you can maintain a balance between caregiving and personal well-being, ensuring both you and your loved one thrive.When to Consider Respite CareRespite care is designed to be flexible and customizable. Whether you need support for a few hours, a few days, or even a few weeks, professional respite care can help you navigate the demands of caregiving without feeling overwhelmed.You should consider respite care if you need to:Take a vacation or a weekend getaway.Attend a business trip or work-related obligation.Run errands or manage household tasks.Recover from an illness, surgery, or injury.Tend to personal matters or simply recharge.While these are all great reasons to seek respite care, the most critical reason is caregiver burnout. When caregiving starts affecting your health, well-being, and ability to provide care, its time to get professional support.The Top 9 Signs of Caregiver BurnoutRecognizing the signs of caregiver burnout is essential for maintaining both your health and the quality of care you provide. If youre experiencing any of the following, it may be time to seek respite care:Feeling OverwhelmedDo you feel like theres too much on your plate? Are household tasks, appointments, and responsibilities piling up? If you constantly feel like youre drowning in to-dos, its a sign that you need support. Respite care can help by giving you time to breathe, regroup, and return to caregiving with renewed energy.Constant ExhaustionFeeling physically and emotionally drained, even after a full nights sleep, is a clear sign of burnout. Caregiving requires a great deal of energy, and without breaks, fatigue can become chronic. Respite care offers you the opportunity to get the rest you need and maintain your health in the long run.Increased IrritabilityIf you find yourself snapping at loved ones, losing patience easily, or feeling frustrated over small things, its a sign that stress is taking its toll. The emotional strain of caregiving can lead to short tempers and strained relationships. Taking a break allows you to reset and approach caregiving with a more positive mindset.Neglecting Your Own NeedsAre you skipping meals, canceling doctors appointments, or not getting enough rest? Many caregivers prioritize their loved ones needs over their own, often at the expense of their health. However, you cant provide the best care for someone else if youre running on empty. Respite care gives you the time and space to take care of yourself, ensuring you stay healthy and strong.ForgetfulnessIf youre forgetting important dates, appointments, or tasks, it may be a sign that stress and exhaustion are affecting your cognitive function. Mental fog and forgetfulness can be dangerous, especially when managing medications or appointments. Taking time to rest and reset can help restore your focus and clarity.Social IsolationWhen was the last time you spent time with friends or did something just for yourself? Caregiving can be isolating, leaving little time for social activities or hobbies. However, maintaining social connections is crucial for emotional well-being. Respite care enables you to step away for a bit and engage with your friends, family, and favorite activities without worry.Concern from Family and FriendsIf your family or friends express concern about your well-being, listen to them. Sometimes, those around us recognize burnout before we do. If your loved ones are urging you to take a break, consider their perspective. Respite care is an easy way to ensure your loved one is well cared for while you recharge.Declining Mental HealthFeelings of sadness, anxiety, or hopelessness should never be ignored. Caregiving can be emotionally taxing, and prioritizing your mental health is just as important as physical health. If you find yourself feeling down, overwhelmed, or unable to enjoy things that once made you happy, respite care can provide the relief you need to focus on your well-being.Making Frequent MistakesMissing medication doses, forgetting doctors appointments, or neglecting essential tasks can have serious consequences. If you notice an increase in mistakes, its a sign that you need to take a step back and recharge. Respite care can help you regain control and ensure that your loved one continues to receive the best possible care.If you recognize any of these signs in yourself, dont wait until burnout takes a toll on your health. Seeking respite care is a proactive step toward maintaining your well-being and ensuring your loved one receives the best possible care. If you have any questions, please call us at 970-240-4121.

10 Activities for Seniors with Dementia or Alzheimers

According to the Alzheimer's Association, it's important to implement routine and creative daily schedules to those who may be dealing with Alzheimer's or Dementia. Routines and creativity can help seniors stay focused, promote relaxation, and decrease the risk of depression. At the same time, one can bring joy, purpose, and positivity to a daily routine.In these routines, there are plenty of ways for family caregivers to cherish great moments and memories together. Start with simple and fun activities that provide joy, mental and physical stimulation, and boost emotional well-being.Keep in mind that the activities may also change according to a senior's mood, physical and mental abilities. It's important to keep having open discussions and list what brings them joy and what they're capable of doing that given day that way, seniors can still have fun and feel engaged. For example, we all know that social interaction is essential, but if an individual is having a more challenging day, consider meeting with smaller circles of people instead of larger social gatherings. It's also important to combine activities inside and outside with a caregiver or loved ones who can help. Here are 10 activities seniors with Dementia and Alzheimer's can do with caregivers or loved ones to bring joy and consistency into their everyday lives: Listen to some favorite music We all appreciate the gift of song. According to the Mayo Clinic, music can also reduce stress by lightening the mood of the caregiver and the senior. If a senior has a particular type of music they enjoy, put an album on and listen with them. Sing along or incorporate a bit of movement for added benefit and fun. Arrange flowers in bouquets As simple as it sounds, arranging flowers in a bouquet is an excellent activity that stimulates positivity and joy. Perfect for those with Alzheimer's or dementia, this activity is creative, stress-free, and engages the mind and brain, reducing agitation and promoting a feeling of safety. Talk about childhood, family, school, or pets Engaging in conversations about pleasant memories encourages self-expression and positive thinking. Asking questions about their childhood or family can support those memories and help a person feel connected to their experiences. And it's great for family bonding. Look at old family photo albums Looking at old family photos can also be an excellent way to bring a senior joy! You can ask them about family members and events or admire the pictures together. Bake cookies or bread It's always nice to have the house smell like baked treats, and the familiar scents of one's favorite bread or cookies can stimulate their senses and make them feel happier. Try making simpler recipes together and put on some music while you bake. Take a walk outside People with Alzheimer's and Dementia need to engage with the outdoors and get in a little bit of exercise, and this activity accomplishes both. Whether it's a walk around the neighborhood or just down the block, getting outside boosts endorphins, which are excellent for reducing anxiousness. Water plants Help a senior feel accomplished and engaged with the outdoors, especially if they can't do strenuous physical activity. Watering plants is another way they can interact with plants and colors. Sit on the porch and drink coffee, hot chocolate, or lemonade Activities don't always have to be "active." Getting out to enjoy a refreshing drink is an easy way to get some fresh air; the taste like the smell is a potent memory booster. Play catch or toss a ball around If a senior can perform slightly more intense physical activities, tossing a ball around in the front or backyard can be a great way to spend time together and exercise. Try tossing a larger, lighter ball that's easier to throw and catch. Do a simple table activity like a puzzle or arrange colored letters Puzzles are excellent brain engagers. You can sit at a table on the porch or in the living room and do a puzzle with fun pictures and colors or arrange colored letters around they don't even have to make words! Fun activities like this ease agitation and provide a feeling of accomplishment. These activities all have a similar goal supporting peace of mind, independence, and engagement while simultaneously providing safety and positivity. Check out our free guides. These guides include scientifically backed statistics, activities, and more, from family caregiver support to information about what to expect as we age.