Understanding your Social Security benefits

Kotler Law Firm P.L.

For more information about the author, click to view their website: Siena Wealth Advisory

Jul 22, 2023

Florida - Southwest

Email US

Click to Email UsWhen it comes to Social Security, there is a lot to consider. Social Security is often associated with a retirement program, but you may enroll if you become disabled or lose a family member. Take a look at the diagrams below for information on how to make the right choices for you and your family.

When should I start collecting Social Security benefits?

The answer is different for every person and depends on many individual factors like your date of birth, marital status and financial position.

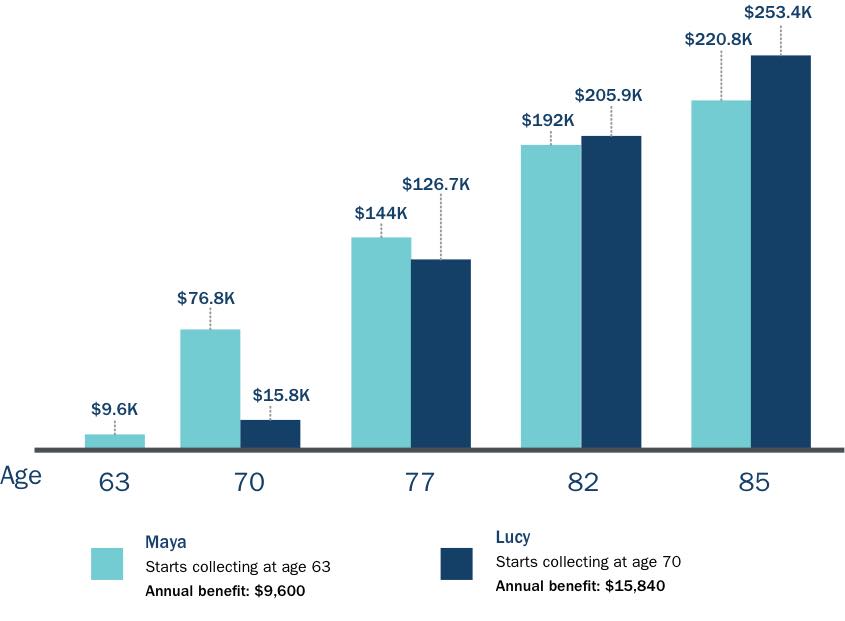

The longer you wait to start collecting Social Security, the higher your monthly benefit will be. An Ameriprise financial advisor can help you determine an appropriate time for you based on your financial situation and goals.

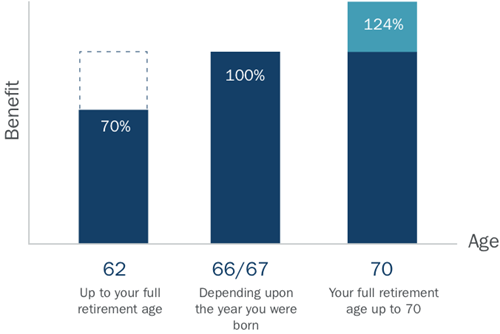

What is my full retirement age?

Your full Social Security retirement age depends on the year you were born. If you were born on January 1 of any year, refer to the previous year to determine your full retirement age.1

How do my Social Security benefits change if I retire early or late?

As life changes and priorities shift, you may wish to retire before or after your full retirement age. Your Ameriprise financial advisor can help you determine an appropriate choice for you. Retiring early locks you into lower monthly payments and will decrease your lifetime benefit amount. Retiring later increases your monthly payment and the amount you will receive over your lifetime.

Can I receive the Social Security benefits of my spouse?

As the spouse of someone receiving benefits, you may be able to claim benefits based on their income, even if you have never worked under Social Security. You may be eligible for benefits if you are:

Can I collect benefits on behalf of my child?

You may be able to claim benefits if the child you are caring for fits the following criteria:

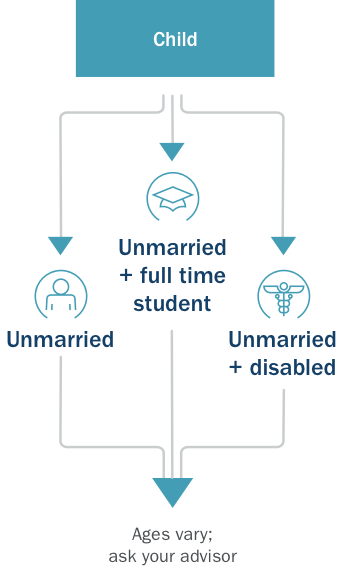

Can my children receive Social Security benefits?

A child who has a parent who is disabled or retired and entitled to Social Security benefits may also be eligible for benefits if they are:

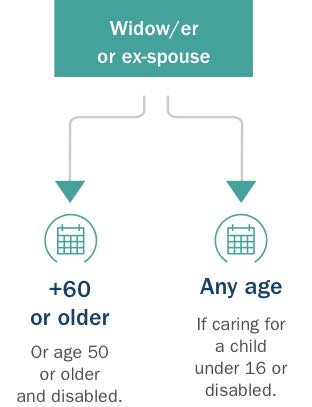

Am I eligible for survivor’s benefits?

You may be eligible for survivor's benefits if you are:

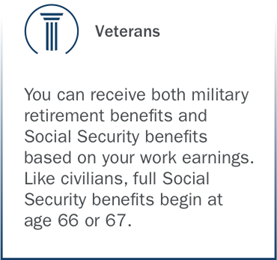

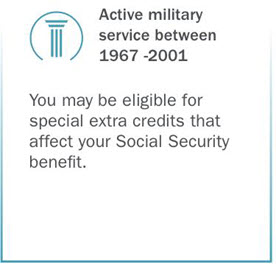

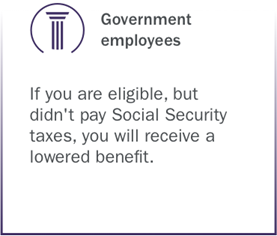

How does my military service or government employment affect my Social Security?

As a veteran or government employee, your Social Security benefits may differ from others:

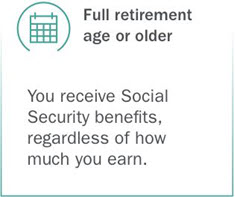

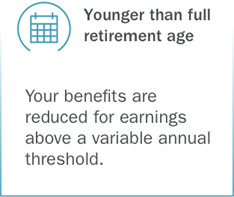

Can I still work and collect Social Security benefits?

You can collect Social Security benefits while working, starting at age 62. However, your age and earnings may impact the amount of benefits you receive during that time. Working won't permanently reduce the Social Security benefits you receive, nor will your withheld benefits disappear.

Once you reach full retirement age:

- Your monthly benefit will increase, taking into account prior benefits detained due to earnings.

- Extra income no longer decreases your benefits.

If you work and collect Social Security when you are:

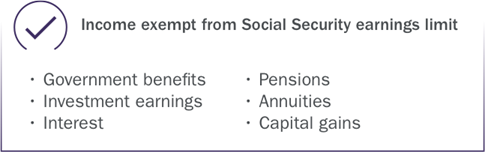

These types of income are exempt from the Social Security earning limit:

*If you work for someone else, only your wage amount applies to earnings limits. If you're self-employed, only your net earnings count.

Does Social Security allow for inflation or cost of living increases?

The Social Security Administration can enact yearly benefit increases called cost-of-living adjustments (COLA) based on inflation. Since 1975, COLAs have ranged from 14.3% (1980) to 0.0% (2009, 2010, 2015). Your financial advisor can help you identify other sources of income when Social security inflation adjustments are low.

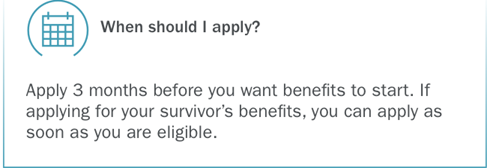

When and how do I apply for Social Security?

An Ameriprise financial advisor can help you navigate the process for Social Security.

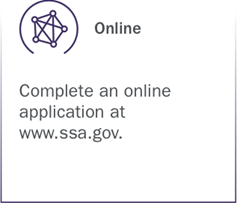

You can currently apply for Social Security in the following ways:

Our advisors can help

If you have any questions about Social Security, your Ameriprise financial advisor can help you understand all aspects of your benefits and help you live more confidently so if your life changes, your plan can too.

- To view the original version of this article visit www.ameriprise.com/financial-goals-priorities/retirement/understanding-social-security

- Seniors Blue Book was not involved in the creation of this content.

Other Articles You May Like

Will My Disability Benefits Change When I Turn 65?

Will My Disability Benefits Change When I Turn 65?Turning 65 years old has traditionally been associated with retirement and enrollment in federal benefit programs. However, people with disabilities may already be receiving federal benefits through Social Security, Medicaid, and Medicare before they turn 65.Disabled individuals who qualify for Social Security Disability Insurance (SSDI) and/or Supplemental Security Income (SSI) may wonder what happens to their disability benefits when they reach retirement age.The short answer is that their benefits dont end, and the amount they received prior to turning 65 remains the same. But given the complexity of the federal benefits system, there may be exceptions to these general rules on a case-by-case basis that need to be discussed with a disability attorney.Age 65 and Full Retirement AgeFor most of Social Securitys history, full retirement age, or the age at which someone could receive the maximum amount of Social Security retirement benefits based on their work history, was 65 years old.Reforms to Social Security in the 1980s raised the full-benefit retirement age to between 66 and 67 years old, depending on when somebody was born. For anybody born in 1960 and later, full retirement age is now 67.When Does Social Security Disability Convert to Regular Social Security?The Social Security Administration (SSA) does not permit a person to receive both disability and retirement benefits on one earnings record at the same time.For anyone receiving SSDI payments, their monthly disability benefit automatically switches to Social Security retirement upon reaching full retirement age. Again, this is age 66 or 67 for most people.When this switch takes place, the monthly payment amount stays the same.How Long Do Social Security Disability Benefits Last?SSDI lasts for as long as the recipient has a disabling condition and is unable to work, or until they reach retirement age, at which time the disability benefit converts to a retirement benefit.Social Security performs a continuing disability review (CDR) of SSDI recipients every three to seven years.Turning 65 or reaching full retirement age does not trigger this review. And once SSDI benefits change over to retirement benefits, there is no need for a medical review, since a recipient doesnt have to be disabled to receive Social Security old age benefits.SSI and Retirement AgeA person may qualify for SSI with a disability if they have little or no income and resources and are age 64 and younger, or they have little or no income or resources and are age 65 and older.Qualifying for SSI does not require a work history the way that SSDI does. So, someone can qualify for SSI without ever having worked. But because the SSI benefit payment is not tied to a work history, SSI benefits do not convert to retirement benefits upon reaching full retirement age.If someones receiving SSI for a disability, their benefits can continue after they reach retirement age as long as they still meet the programs financial requirements.Disabled SSI recipients are subject to a CDR at least once every three years, or every five to seven years. During the CDR, the SSA also reviews a recipients income and resources to ensure they are still eligible for and receiving the correct SSI benefit amount.Disability, Medicare, and Turning 65Medicare eligibility ordinarily begins at age 65. But people under age 65 whove gotten SSDI benefits for at least 24 months can start receiving Medicare.SSDI recipients automatically get Medicaid Part A and Part B, collectively known as Original Medicare, after receiving their 25th month of benefits. They can choose at that time to decline or keep Part B, which covers services from doctors and other health care providers. They must typically keep Part A, the portion covering inpatient hospital care.When individuals with qualifying disabilities turn 65 and gain age-based Medicare eligibility, they dont have to re-enroll or complete additional paperwork to continue receiving health care benefits.Turning 65, though, amounts to a secondary initial enrollment period. This could be a good time to re-evaluate current Medicare coverages and make changes.For example, a disabled Medicare recipient may have declined Part B coverage when they first enrolled but decide to keep this coverage when they enroll again at age 65. They can also choose to enroll in another Medicare program, such as Part C or D.Disability, Medicaid, and Turning 65Medicaid is government health care for people with limited income, including those with disabilities.In many states, SSI recipients automatically qualify for Medicaid. Medicaid eligibility thats based on receiving SSI should not be impacted by turning 65, but there could be considerations related to special needs trust funding at age 65.Medicaid covers some costs that Medicare does not, such as long-term care. Special needs trusts can help to preserve a beneficiarys access to benefits like SSI and Medicaid. But the window of time to fund a first-party special needs trust closes at age 65.Some people are also eligible for both Medicaid and Medicare. They may be able to enroll in a Dual Eligible Special Needs Plan, a type of managed care plan that helps to coordinate coverage for those with complex medical needs.Work With a ProfessionalSSDI, SSI, Medicare, and Medicaid all have complex rules that may vary by state. Whether youre turning 65 or reaching retirement age, contact Ashley Day at 251-277-3377. She can provide answers and assist with any necessary paperwork.

Take Control of Your Finances: 7 Budgeting Tips for Seniors

Managing your finances can feel daunting, especially as lifes expenses add up. But with the right strategies, you can take control, stretch your dollars, and enjoy peace of mind. Here at Seniors Helping Seniors, we believe financial independence is empowering, and were here to help! From grocery savings to solar panels, these practical tips will guide you toward a brighter, more secure future.1. Shop Smart and Save at the Grocery StoreMany grocery stores offer senior discountsan easy way to save on everyday essentials. Pairing these discounts with meal planning can help stretch your weekly budget. Need a hand? A Seniors Helping Seniors caregiver can assist with planning nutritious meals while keeping costs down.2. Tap Into Free or Low-Cost Community ResourcesYour community likely offers a variety of free or low-cost services designed for seniors. Think meal delivery programs, recreational activities, or transportation services. Staying active and connected doesnt have to break the bank, and these resources can add tremendous value to your lifestyle without adding to your expenses.3. Take Advantage of Senior DiscountsFrom restaurants to retail stores, discounts for seniors are everywhere! Many establishments offer lower prices or special deals for older adults. Whether its a favorite coffee spot or a hardware store, these small savings add up, making it easier to enjoy your favorite things while staying within your budget.4. Use a Budgeting App to Track Your SpendingSimplify money management with a budgeting app. These tools make it easy to monitor your spending on groceries, utilities, entertainment, and more. If technology feels overwhelming, your caregiver can guide you through setup and show you how to track your finances effectively. Its a small step that leads to big financial clarity.5. Automate Savings and Bill PaymentsAvoid late fees and grow your savings by automating your finances. Set up automatic transfers to your savings account or schedule recurring bill payments through your bank. This hassle-free approach helps ensure your bills are always paid on time, leaving you more time to focus on what matters most.6. Work With a Caregiver for Personalized SupportA Seniors Helping Seniors caregiver can be your budgeting buddy. From spotting local discounts to helping you navigate government programs, your caregiver can provide personalized assistance. Together, you can create a financial plan that fits your needs, so you can spend less time worrying and more time enjoying life.7. Save on Energy with Solar PanelsIf youre ready to invest in long-term savings, consider solar panels. They harness renewable energy, reducing your electricity bills and your carbon footprint. With available tax credits and rebates, going solar might be more affordable than you think. Plus, its a great way to contribute to a greener planet.A Brighter Financial Future AwaitsYour golden years should be filled with joy, not financial stress. These tips are designed to help you budget smarter and save more, empowering you to live life fully and confidently. If youre feeling overwhelmed, our Seniors Helping Seniors team is here to help. With expert guidance and a caring approach, well work alongside you to create a plan that fits your life.Lets tackle those finances togetheryouve got this!Seniors Helping Seniors Making Life Easier, One Step at a TimeFor more tips and support, visit our website or contact your local Seniors Helping Seniors office.

Turning 65? Avoid Paying a Medicare Penalty

WHEN TO ENROLL IN MEDICARE TO AVOID PAYING PENALTIESIf youre turning 65 soon, youve hopefully started your personal Medicare journey. Theres a lot of information, and it can be confusing. A valuable service by Millennium Physician Group is our Millennium Medicare Connect program. It delivers access to programs, network, and doctors that give you the confidence to make the right Medicare choices and the tools to get the most out of your healthcare.If you dont sign up for Medicare when youre first eligible or pick up Part B within 60 days of retirement, you may incur a late enrollment penalty that will stay with you every year, explains Valentina Ayala, a Medicare Advisor from HealthShare360.IF YOURE TURNING 65 AND NO LONGER PLAN TO WORK:You should enroll in Medicare Part B to avoid paying a penalty for late enrollment. Part B is the medical insurance (or doctor coverage) youre entitled to. It requires a monthly premium, and you have a limited time to sign up. If not, you could delay your coverage until the following year.IF YOURE TURNING 65 AND PLAN TO CONTINUE WORKING:If you (or your spouse) are still working, Medicare works a little differently. It depends on how you currently get your health insurance and how many employees there are in your company. There are a lot of variables, so its recommended you talk to an unbiased, qualified expert in Medicare plans and options to determine how you get Medicare based on your situation.IF YOUVE RETIRED BUT ARE GOING BACK TO WORK:If you can get employer health coverage thats considered acceptable as primary coverage, you are allowed to drop Medicare and re-enroll later without penalties, or you can use it as your secondary coverage.Every situation is unique, which is why I encourage [people] to talk to an insurance agent specializing in Medicare about your plan options to help you enroll in the plan thats best suited for your individual needs, says Ayala.Millennium physicians lead the country in the quality of care they deliver to Medicare patients. To find out more about your Medicare options, including connecting with our Medicare Advisors, visit YourMedicareConnect.com.