Your Estate Plan Checklist

Advocate In-Home Care - Ft. Myers

Oct 18, 2022

Florida - Orlando , Florida - Sarasota, Bradenton & Charlotte Counties , Florida - Southwest

Email US

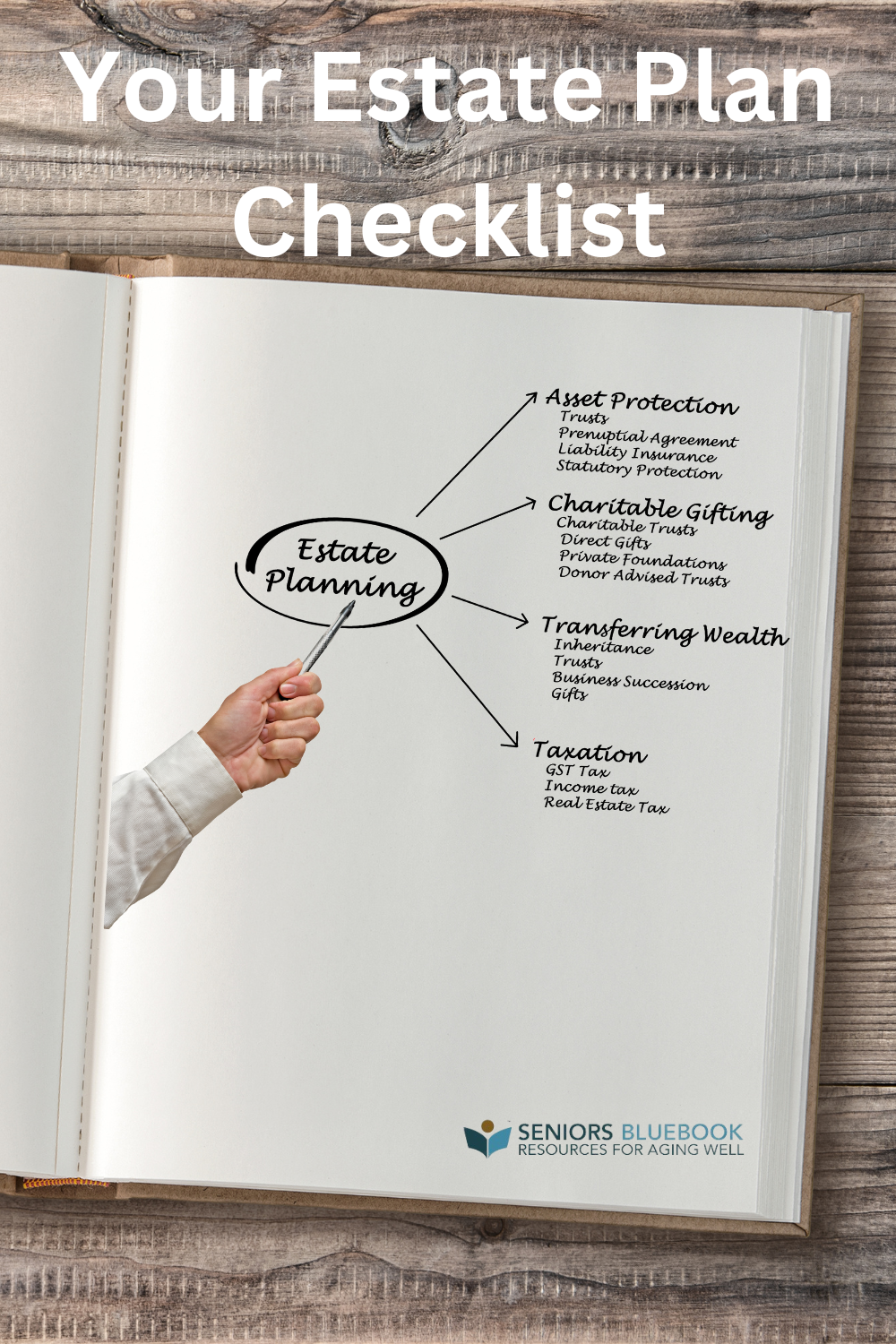

Click to Email UsEstate plans are a common way for Americans to get all of their assets in order, especially as they age. However, most people's plans are incomplete and often don't address some of the most important subjects.

This estate plan checklist will help you ensure that you have a sound estate plan. However, you should also look into getting an attorney who specializes in elder law, and a financial analyst to help ensure that your plan and your assets are protected and being managed properly. The National Academy of Elder Law Attorneys is a great resource to find an attorney in your area that meets your needs.

1. Will

A will provides instructions for distributing your assets to your family and other beneficiaries when you pass. Your will also appoints someone to be the executor to pay final expenses, taxes, etc., and then distribute the remaining assets. If you have minor children, a will is also a way to designate a guardian for them. A won’t take effect until you die, and it cannot provide for management of your assets if you become incapacitated. That’s why it is necessary to have other estate planning documents in place to utilize if you should be unable to act for any reason.

2. Durable power of attorney for business and health care decisions

A power of attorney is a legal document in which you name another person to act on your behalf. You can give this person/agent broad or limited powers. You should choose this person carefully because he or she will be able to sell, invest and spend or distribute your assets. A durable power of attorney continues to apply if you are incapacitated and terminates only upon your death, whereas a traditional power of attorney terminates upon your disability or death.

3. Health care power of attorney and living will

A health-care power of attorney authorizes a person you designate to make medical decisions for you in the event you are unable to do so yourself. This document, coupled with a living will are necessary to avoid family conflicts and even court intervention should you become unable to make your own health care decisions. A living will dictate your wishes regarding the use of life-sustaining treatments and other end-of-life medical care in the event of a terminal illness or accident. It states what you do and do not want done in terms of treatment but doesn’t give any individual the legal authority to speak for you. That is why it is usually coupled with a health care power of attorney.

4. Revocable living trust

You’ll need one of these to transfer, manage and distribute assets while you are alive and to avoid probate after your death. There are many different kinds of trusts, which are usually put in place to minimize estate taxes. Each trust has benefits and should be discussed with your attorney. There are marital trusts, charitable trusts, generation-skipping trusts, bypass trusts, testamentary trusts, qualified terminable interest property trusts, and more. A revocable living trust is often used in estate plans. By transferring assets into a revocable living trust, you can manage your financial affairs during your lifetime and provide management if you become incapacitated. A revocable living trust lets trust assets avoid probate, keeps personal information private and can designate the disposition of trust assets to future generations.

5. List of Assets

A list of assets will serve as a guide for those managing your estate or your affairs if you are incapacitated. Use this form from Retired Brains to list all your assets and where they are located.

6. Do not Resuscitate Order (DNR)

A DNR medical order written by a doctor instructs any healthcare providers to not use cardiopulmonary resuscitation (CPR) if a patient stops breathing or heart stops beating. Some feel this is an important document, while others do not. If it is important to you, include this document in your plan.

7. Legacy Letter

A legacy letter is an ethical will designed to pass “ethical values” from one generation to the next. Traditional wills involve what you want your loved ones to have. Ethical wills involve what you want your loved ones to know.

8. Discussion with attorney about who inherits what assets

Decide where you want your assets to go and discuss this specifically with your attorney.

9. Selection of someone to make medical decisions if necessary

Decide whom you want to make health decisions on your behalf if you are incapacitated.

10. Instructions on how you want your assets distributed

Have this discussion with your attorney and/or spouse or appropriate family member, trustee, etc.

11. Guardian decision

If you have minor children, you may wish to name a guardian to take care of them in the event of your passing.

12. Estate plan tax review

Meet with your accountant and attorney to discuss the tax consequences of your estate plan.

13. Instructions on how to handle digital legacy

Check your digital footprints. Most people aren’t aware of the full extent of their presence online. List any personal sites and review the steps necessary to protect online information after your death or if you are no longer able to act on your own behalf.

14. Letters to your family

Consider writing a letter to your spouse or family regarding your funerary wishes should you need to be removed from life support or pass unexpectedly. This letter will make their decisions a great deal easier if you reiterate that this is your wish with a personal, not formal, request.

Other Articles You May Like

Estate Planning in the Western Slope of Colorado: A Vital Step for Seniors and Families

Planning for the future is one of the most important things we can do for our loved onesand ourselves. In the Western Slope of Colorado, estate planning is an essential step for seniors who want to ensure their wishes are respected, their assets are protected, and their families are supported.Whether you're just beginning to explore estate planning or looking to update an existing plan, this guide will help you understand the key components of estate planning and how to access helpful local resources in the Western Slope area. What Is Estate Planning?Estate planning is the process of arranging for the management and distribution of your assets and responsibilities in the event of your death or incapacitation. Its not just for those with large estatesestate planning is a smart and necessary step for anyone who wants to:Protect property and financial assetsEnsure their wishes are followedMinimize family disputesAppoint guardians for dependentsPlan for healthcare decisionsA well-crafted estate plan typically includes documents like a will, trust, durable power of attorney, and advance healthcare directive. Why Estate Planning Matters for SeniorsAs we age, the need for legal and financial clarity becomes increasingly important. Estate planning provides peace of mindnot only for the person making the plan but for their family members as well.In the Western Slope region, where many seniors value independence and community, estate planning is especially helpful in addressing:Long-term care considerationsAsset protection for loved onesTransferring property, land, or family businessesCharitable givingReducing estate taxesBy planning ahead, seniors can avoid unnecessary legal complications and protect the legacy they've worked hard to build. Estate Planning Resources in the Western Slope of ColoradoThe Western Slope encompasses a diverse and vibrant part of Colorado, with strong local support networks for seniors and their families. Estate planning services in this area range from elder law professionals to non-profit legal aid and senior resource centers.Start your search here: Explore Senior Resources in the Western Slope Browse Estate Planning Services in the Western SlopeBe sure to look for services that offer:Experience working with seniorsCompassionate, clear communicationTransparent pricing or sliding-scale feesEducational workshops or free consultations Key Components of a Strong Estate PlanIf you're working with a legal professional or starting a DIY plan, make sure to include these essential pieces:Will: Outlines how your property should be distributed and who will serve as guardian for any dependents.Trust: Helps manage and distribute assets while potentially avoiding probate.Durable Power of Attorney: Authorizes someone to manage your finances if you're unable to do so.Advance Healthcare Directive: Specifies your medical care preferences and names someone to make decisions on your behalf if necessary.Beneficiary Designations: Ensures your life insurance, retirement accounts, and other policies are up to date.Even small updateslike changing a beneficiary or updating an addresscan make a big difference when the time comes. Local Insight: Estate Planning in Rural and Mountain CommunitiesOne of the unique aspects of estate planning in the Western Slope is the variety of property types and lifestyles. Many residents own land, ranches, or vacation homes, which require special attention in estate documents. Its also common for families to live in multi-generational households or have long-standing ties to their community.Working with a professional who understands the local context and real estate laws in Colorado is important for ensuring your estate plan is legally sound and culturally sensitive. Final ThoughtsEstate planning isnt just about preparing for the endits about creating a legacy, protecting your loved ones, and maintaining control over the decisions that matter most to you. If youre ready to begin or revisit your estate planning journey, the Western Slope offers trusted professionals and community resources to support you along the way. Taking action now can ease the burden on your family and give you confidence about the future.

Estate Planning in Utah: Why Its Essential for Seniors and Their Families

Planning for the future isnt always easybut for seniors in Utah, estate planning offers peace of mind, protects assets, and ensures your wishes are honored. Whether you live in Salt Lake City, St. George, or Provo, having a thoughtful estate plan is one of the most important steps you can take to safeguard your legacy.In this guide, well break down the essentials of estate planning in Utah, explain why its so critical for seniors, and share trusted local resources that can help. What Is Estate Planning?Estate planning is the process of legally documenting your wishes for how your assetssuch as property, investments, savings, and personal belongingswill be managed and distributed after your death or in the event you become incapacitated. A comprehensive estate plan may include:A willA revocable living trustPowers of attorney (medical and financial)An advance healthcare directiveGuardianship designations (if applicable)In Utah, estate planning can also help your family avoid probate court, reduce estate taxes, and prevent disputes that could arise without clear legal guidance. Why Estate Planning Matters for Seniors in UtahUtah is home to a growing senior population who value independence, family, and financial security. Heres why estate planning should be a priority:1. Protect Your Loved OnesWithout an estate plan, the courts will determine how your assets are divided. This often leads to confusion or conflict among family members. Having a plan in place ensures your intentions are followed.2. Avoid Probate DelaysProbate can be a lengthy and costly process in Utah. Tools like living trusts help avoid probate and allow for a faster, smoother transfer of assets to your beneficiaries.3. Plan for IncapacityAn estate plan isnt just about what happens after you passits also about who will make decisions for you if you're unable to. Assigning a trusted medical and financial power of attorney ensures your wishes are respected during a medical crisis.4. Support Charitable CausesMany Utah seniors wish to leave a legacy by supporting local causes. Through estate planning, you can designate charitable organizations to receive a portion of your estate, ensuring your values live on. Utah-Specific Considerations for Estate PlanningUtah estate law has unique aspects that seniors and families should understand:Spousal Elective Share: Utah law ensures that a surviving spouse receives a share of the estateeven if not explicitly mentioned in the will.Simplified Probate for Small Estates: Utah allows for a simplified probate process for estates valued under a certain threshold.Digital Assets: Utah law includes provisions for managing digital assets (like online accounts) as part of your estate.Its important to work with professionals familiar with Utah laws to ensure your estate plan is legally sound. Trusted Estate Planning Resources in UtahFinding the right professionals and support is essential for successful estate planning. SeniorsBlueBook.com offers a curated directory of trusted senior resources in Utah, including those who can assist with legal, financial, and end-of-life planning needs.You can also explore this specific category to find Estate Planning and Elder Law specialists in Utah who understand the unique needs of aging adults and their families. Start Your Estate Planning Journey TodayIts never too earlyor too lateto begin planning for your future. Whether youre updating an old will or creating a comprehensive estate plan from scratch, taking the first step ensures that your wishes are documented and your loved ones are supported. Remember, estate planning is more than a legal task. Its a gift to your family, a declaration of your values, and a way to take control of your future.

Understanding Assisted Living in Utah: A Comprehensive Guide for Families

As Utahs population continues to age, many families are exploring senior living options that provide both independence and essential support. Assisted living is one of the most sought-after solutions, offering a balanced environment for seniors who need help with daily activities but still wish to maintain a sense of autonomy. If you're beginning the search for assisted living in Utah, understanding what these communities offer and how to choose the right fit is essential.This guide will help you navigate assisted living in Utah with clarity, confidence, and compassion. What Is Assisted Living?Assisted living refers to a residential community designed for seniors who are largely independent but may need assistance with tasks like bathing, dressing, medication management, or meal preparation. Unlike skilled nursing facilities, assisted living communities do not provide round-the-clock medical care, but they do offer 24/7 supervision and support from trained staff.Most assisted living communities in Utah also offer amenities such as:Private or semi-private apartmentsGroup dining with nutritious mealsHousekeeping and laundry servicesTransportation assistanceRecreational and social activitiesOn-site wellness programs Why Utah Families Choose Assisted LivingUtah has become a popular place for retirees and seniors due to its beautiful landscapes, relatively low cost of living, and strong sense of community. Assisted living communities in Utah often incorporate the natural beauty of the state, offering seniors a lifestyle thats both safe and enriching.Some key benefits of assisted living in Utah include:Peace of Mind for Families: Knowing your loved one is in a secure and supportive environment can ease the burden of caregiving and reduce family stress.Tailored Care: Assisted living communities evaluate each residents unique needs and develop a personalized care plan to support their independence and health.Social Opportunities: Many Utah seniors face isolation, especially in rural areas. Assisted living communities encourage social interaction, which is essential for mental and emotional well-being.Access to Nature and Recreation: Utahs outdoor culture often extends into its assisted living communities, offering residents scenic views, walking paths, and outdoor events. How to Choose an Assisted Living Community in UtahWhen selecting an assisted living community for yourself or a loved one, consider the following factors: Level of Care: Ensure the community can accommodate current needs and adapt to future care requirements. Licensing and Accreditation: Verify that the community meets Utahs health and safety regulations. Location: Proximity to family, medical providers, or familiar neighborhoods can make the transition smoother. Costs and Contracts: Understand the fee structure, what's included, and any additional costs. Culture and Environment: Visit communities in person or virtually to observe how staff and residents interact, and assess whether the atmosphere feels welcoming and respectful. Finding Assisted Living Communities in UtahSeniors Blue Book is a trusted resource for families exploring senior care options across Utah. Our comprehensive directories help you compare services, amenities, and locationsall in one place.To start your search, explore these helpful pages:Utah Senior Housing DirectoryAssisted Living Communities in UtahThese listings are updated regularly and include detailed profiles of local providers, ensuring you have accurate information to make informed decisions. Final ThoughtsChoosing assisted living is a major life decision that can significantly enhance the quality of life for Utah seniors and provide much-needed relief for their families. Whether youre just beginning your research or ready to schedule tours, understanding your options is the first step toward a supportive and fulfilling future. Assisted living in Utah offers more than just careit offers community, dignity, and peace of mind. Start exploring your options today with help from the Seniors Blue Book.