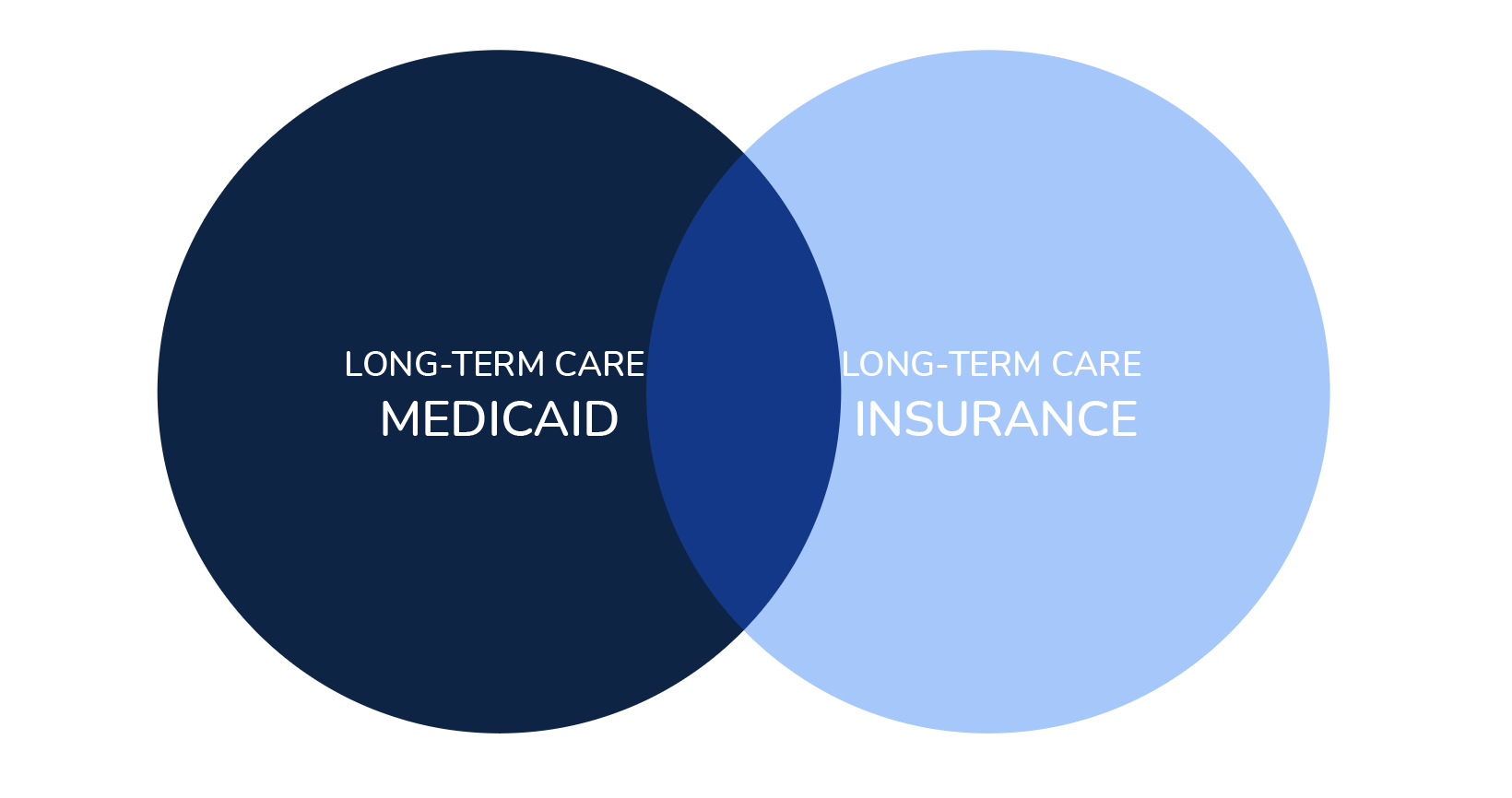

Long-term Care Medicaid vs Insurance: What's the Difference?

Beneficent: LTC Funding Education & Options

For more information about the author, click to view their website: Beneficent - LTC Options

Apr 20, 2023

Email US

Click to Email Us5 Minute Read

Understanding Long-Term Care Medicaid and Insurance

The #1 cause for people filing for bankruptcy due to medical bills.

“A new study from academic researchers found that 66.5 percent of all bankruptcies were tied to medical issues.” Therefore, the cost of long-term care is often a major concern for families. When it comes to managing the costs associated with long-term care, there are 2 primary options available to individuals and families.

- Long-term Care Medicaid

- Long-term Care Insurance

Before deciding which option is the best fit, it’s important to understand the differences between these two types of coverage. Read on to learn more about understanding Long-term Care Medicaid and Insurance.

Long-term Care Medicaid

Long-term care Medicaid is a government program that provides medical and related services for people who meet certain income and resource requirements. This program is jointly funded by state and federal governments, so the details can vary from state to state. In general, eligibility requirements include being over 65 years old, blind or disabled and needing help with more than 2 of the activities of daily living. (Activities of daily living examples – getting dressed, bathing, cooking, and more.) In some cases, individuals may be eligible for Long-term Care Medicaid even if their income and resources exceed the eligibility limits.

Long-term Care Insurance

In contrast to Long-term Care Medicaid, Long-term care insurance is an individual policy that you purchase from an insurance company. This type of coverage pays for custodial services such as assistance with activities of daily living like bathing and dressing as well as inpatient nursing home stays up to a predetermined amount per day. It can also cover other professional services like adult daycare programs or home health aides. Depending on your policy, you may also be eligible for additional benefits such as mental health treatment or respite services for family members who are providing care at home.

Pros and Cons

Many people find that they cannot afford the high premiums associated with Long-term Care Insurance, and Medicaid is a great option when it comes to paying for long-term costs. Preexisting conditions may also hinder an applicant’s ability to attain a Long-term Care Policy. With a lot of misinformation, many people also find it hard to determine if they are even eligible for Medicaid.

Deciding which type of coverage—Long-term Medicaid vs Insurance—is right for your situation can be difficult because of their complexities. Both options have their pros and cons but understanding them both can help guide you toward making an informed choice about how best to manage the costs associated with long-term care. Need to determine if you are eligible for Medicaid? Meet with Stacy Osborne, a Medicaid Certified Planner. In 1 hour, you will walk away with a Long-term Care plan in place at no charge.

Stacy Osborne, MBA, CMP

Stacy Osborne, MBA, CMP

Beneficent CEO

719.645.8350

Other Articles You May Like

Creating a Safe and Comfortable Mother-in-Law Suite for Senior Living at Home

Home is more than a buildingits a place where milestones are celebrated, bonds are strengthened, and everyday life unfolds. For families in Western Colorado, keeping senior loved ones close to home is often the ideal choice. One increasingly popular solution is the creation of a mother-in-law suite, also known as an in-law apartment or private living space for aging parents.These thoughtfully designed suites offer seniors the best of both worlds: privacy and independence combined with the security, connection, and warmth that come from being near family. For many households, they provide an effective way to balance care needs with lifestyle preferences, making it easier for older adults to remain safe and engaged while still enjoying their own personal space.Is a Mother-in-Law Suite Right for Your Family?Every family faces unique circumstances when it comes to senior care. Some older adults require only minimal support, while others need daily assistance with mobility, personal care, or health management. A private in-home suite can meet both needs by allowing independence while ensuring safety measures and family support are always nearby.If your loved one values autonomy but still benefits from a protective environment, this type of arrangement can offer the perfect blend of comfort, security, and peace of mind.Features That Enhance Senior LivingBalancing Privacy and TogethernessTransitioning into a family members home is a major adjustment, and many seniors fear becoming a burden. A dedicated suite helps address these concerns by creating a private retreat within the home.Design options might include: A separate entrance for added independence Soundproofing to allow quiet and privacy A cozy sitting area for reading or relaxation Additional features, such as a kitchenette for preparing light meals or shared outdoor spaces like gardens and patios, allow seniors to maintain independence while staying connected to family life. Integrating smart technologies such as intercom systems or video doorbells also boosts both security and convenience.Putting Safety FirstSafety is at the heart of any senior living design. Falls remain one of the most common risks for older adults, but a home thats built or modified with these challenges in mind can significantly reduce that risk.Helpful safety modifications may include: Grab bars in bathrooms and near entryways Walk-in showers or tubs with low thresholds Non-slip flooring in high-traffic areas Sturdy railings on stairs and ramps Even small upgrades can make daily routines easier and safer. According to the CDC, about one in four older adults experiences a fall each year, making preventative measures essential.Lighting That Works for Safety and ComfortProper lighting not only prevents accidents but also makes a suite feel inviting. Bright, warm spaces encourage activity and enhance mood.Some effective options include: Motion-sensor lighting in hallways and bathrooms Task lighting in kitchens and workspaces Under-cabinet fixtures for added visibility Adjustable smart lighting systems for day and night comfort Pairing upgraded lighting with fresh, lighter paint colors can also brighten a suite, making it both functional and cheerful.Planning for the FutureWhen creating a mother-in-law suite, its wise to think ahead. Even if a loved one is fully mobile today, needs may change over time. Designing for aging in place ensures the space remains functional in the years to come.Future-ready features might include: Wider doorways for walker or wheelchair access Step-free entries and smooth flooring transitions Lever-style handles instead of traditional knobs Extra built-in storage for medical or mobility equipment These improvements not only support long-term comfort but can also increase the overall value of the home.More Than Safety: Creating a Joyful Daily LifeWhile safety is essential, senior living should also be enjoyable and fulfilling. A mother-in-law suite provides the foundation for independence, but daily experiences within that space truly shape quality of life. Simple activitiessharing a favorite hobby, cooking a meal together, or enjoying a walk outdoorshelp seniors feel connected and purposeful. Designing spaces that support these moments makes life richer for everyone involved.

NEW Colorado Home Care Program: What You Need to Know

IntroductionStarting July 1, 2025, Colorado launched a new home care program through Medicaid called Community First Choice (CFC). This program is designed to help people who qualify for Long-term Care Medicaid stay safely in their own homes instead of moving into a nursing facility. Its one of the biggest changes to Colorados Medicaid long-term care system in years, and it may open new options for your family.At Beneficent, we know these programs can feel confusing. Below, well break down the essentials in plain language so you can decide whether this program might help your loved one.What Is the New Program?Community First Choice (CFC) is a new benefit under Health First Colorado (Medicaid). It gives people who need daily help access to in-home caregivers and supports. Think of it as a way to get the same kind of personal care someone might receive in a nursing home but delivered right at home.Who May Qualify?Your loved one may be eligible if they:Are already on Health First Colorado (Medicaid)Need help with everyday activities at the level a nursing facility would provide (for example, assistance with bathing, eating, mobility, or medication reminders)If your loved one is already on a Medicaid waiver, they can transition to this program during their annual review.What Services Can Families Expect?Families can expect support that makes day-to-day living easier and safer, such as:Personal Care help with bathing, dressing, using the restroom, eating, and moving around safelyHomemaker Services light cleaning, laundry, meal prep, and errands like grocery shoppingHealth-Related Support medication reminders, wound care, and teaching daily living skillsSafety Technology personal emergency response buttons, medication reminders, or home-delivered mealsTransition Assistance covering move-in costs if someone is moving out of a facility back into the communityHow Services Are DeliveredOne of the biggest benefits of this new program is choice:You can use an agency, which sends licensed caregivers to the home.Or, you can direct the care yourself hiring and managing your own caregiver (sometimes even a trusted family member).This flexibility gives families more control over who provides care and how its done.Why This Matters for FamiliesNo waitlists: Unlike many waiver programs, CFC is an entitlement. If your loved one qualifies, they can begin receiving services right away.More independence: This program is designed to help people remain at home, surrounded by family, rather than in a facility.Financial relief: Medicaid covers the costs, easing the financial burden on families who may otherwise struggle to afford care.How to Get StartedIf youre wondering whether your loved one may qualify, here are next steps:At Beneficent, we specialize in helping families understand programs like this, navigate the paperwork, and secure approval as quickly as possible. Schedule an initial consult here. doinggoodforothers.com/schedule-a-free-consultationFinal ThoughtsColorados new home care program (CFC) is a positive step for families offering more flexibility, quicker access to services, and the ability for loved ones to remain at home.If youre unsure whether your parent or loved one qualifies, reach out. Well walk you through eligibility, and help manage the application process from start to finish.

Blissed to Assist: Personal Assistance for Busy Lives in Fort Collins and Northern Colorado

Life today moves fast. Between managing careers, nurturing families, and maintaining personal well-being, many people feel stretched thin. For busy professionals, families, and seniors alike, there never seem to be enough hours in the day to handle it all. Thats where Blissed to Assist comes in. Based in Fort Collins and proudly serving Northern Colorado, Blissed to Assist offers personalized support services designed to simplify life, restore balance, and free up your valuable time.Whether you need organizational help, day-to-day assistance, or someone you can count on to keep life running smoothly, Blissed to Assist provides trusted solutions with a personal touch.The Vision Behind Blissed to AssistThe inspiration for Blissed to Assist came directly from the lived experiences of owner and founder, Lauren Bussey. While balancing the demands of a directorship role, pursuing another degree, nurturing personal relationships, and managing family responsibilities, Lauren found herself in a position familiar to manyoverwhelmed and in need of support.What she discovered was a gap in available services. While there were options for task-specific help, there was no comprehensive, compassionate, and customizable support tailored to professionals, families, and seniors juggling diverse needs. Instead of settling, Lauren turned her challenge into an opportunity.Drawing from her background as a caregiver, educator, and executive, Lauren built a business rooted in her own values of integrity, compassion, safety, adaptability, respect, and excellence. Today, Blissed to Assist continues that mission: to empower clients by providing the very type of personal assistance she once needed herself.About the Owner: Lauren BusseyLauren is more than an entrepreneurshe is a caring professional who understands firsthand the weight of competing responsibilities. Her personal and professional journey uniquely prepared her to create Blissed to Assist, a service that blends practical solutions with genuine compassion.Outside of work, Lauren lives a fulfilling life as a proud pet mom and an adventurer at heart. She enjoys spending time with family and friends, attending live concerts, skiing, kayaking, cooking, and horseback riding. Her zest for life and wide range of interests shine through in the way she connects with her clientsbringing empathy, energy, and balance to every interaction.Tailored Services for Every LifestyleAt Blissed to Assist, no two clients are alike. Thats why every service is tailored to individual needs, ensuring support that fits seamlessly into your life. Services are available in both in-person and virtual formats, offering flexibility for modern schedules.Here are some ways Blissed to Assist can help:For Busy Professionals Time management & scheduling support so you can focus on what matters most. Organizational solutions for both work and home life. Errand running & task management to take care of the details that weigh you down. Virtual administrative support for emails, scheduling, and project coordination. For Families Household organization to bring structure and peace of mind to busy homes. Errands & shopping assistance for everything from groceries to appointments. Support for parents juggling multiple responsibilities, ensuring no task gets overlooked. Coordination of family activities or schedules for smoother daily routines. For Seniors Compassionate companionship to reduce feelings of isolation. Assistance with appointments, errands, and household tasks to promote independence. Personalized organization solutions to create a safe, comfortable home environment. Flexible, respectful support that honors dignity and enhances quality of life. Whether its streamlining your office workload, organizing your home, or providing reliable personal support, Blissed to Assist creates a custom plan designed to fit your unique lifestyle.Why Choose Blissed to Assist?In a world of generic service providers, Blissed to Assist stands apart. Heres why clients across Northern Colorado trust Lauren and her team: Locally Owned & Independent As a Fort Collinsbased business, Blissed to Assist understands the local community and provides personalized care that national companies simply cant match. Values-Driven Service Integrity, compassion, adaptability, and excellence guide every client interaction. Comprehensive Support From small daily tasks to larger organizational projects, no need is too big or too small. Customized Approach Every client receives a plan built specifically for them, ensuring meaningful results. Safety & Trust Your comfort, privacy, and peace of mind are always the top priorities. Serving Fort Collins and Northern ColoradoBlissed to Assist is proud to serve Fort Collins, Loveland, Greeley, Windsor, and the greater Northern Colorado area. As a region known for its blend of vibrant city life and outdoor adventure, Northern Colorado attracts busy professionals, growing families, and retirees alike. Blissed to Assist offers the support needed to help each of these groups live fully and stress-free.Whether youre navigating the fast-paced environment of a career, seeking balance for your household, or looking for extra support as a senior, Blissed to Assist is your trusted partner.The Bigger Picture: A Life Well-LivedAt its core, Blissed to Assist is about more than just completing tasksits about helping people reclaim their time, energy, and peace of mind. With reliable assistance and compassionate service, clients are free to focus on what truly matters: building careers, making memories with family, enjoying hobbies, or simply embracing more balance in everyday life.By stepping in where needed, Blissed to Assist gives clients the gift of a life less cluttered and more fulfilling.Get Started TodayIf youve ever felt the stress of too many responsibilities and not enough hours in the day, youre not aloneand you dont have to do it all by yourself. Blissed to Assist is here to simplify life and provide the personalized support youve been searching for.Discover how Blissed to Assist can help you: Regain valuable time Reduce stress Stay organized Enjoy more of the life youve worked hard to create Serving Fort Collins and all of Northern Colorado, Blissed to Assist is ready to be your trusted partner in creating a more organized, efficient, and joyful daily experience.Final ThoughtsOwner Lauren Bussey founded Blissed to Assist because she knew the need for reliable, tailored personal assistance was real. What started as a solution for her own overwhelming schedule has grown into a business dedicated to helping others live with more ease and fulfillment.With services rooted in care, trust, and flexibility, Blissed to Assist is more than a service providerits a partner in your journey toward balance and well-being. Take the first step today. Regain your valuable time, and let Blissed to Assist support you in creating the life you deserve.

Local Services By This Author

Beneficent: Learn How to Pay For Long-Term Care

Medicaid Planning 665 Southpointe Court, Colorado Springs, Colorado, 80906Beneficent creates solutions for senior and disabled adults to pay for Long-term Care Services - INCLUDING HOME CARE, ASSISTED LIVING, OR SKILLED NURSING. Our clients benefit from step-by-step guidance which results in minimizing spend down, preserving assets, and limiting out-of-pocket expenses. BENEFICENT HAS OVER 200 FIVE-STAR REVIEWS ON GOOGLE AND THE BETTER BUSINESS BUREAU. During our FREE initial consultation, you'll walk away with certainty on your next steps moving forward regarding how to pay for long-term care.